Page 48 - International Taxation IRS Training Guides

P. 48

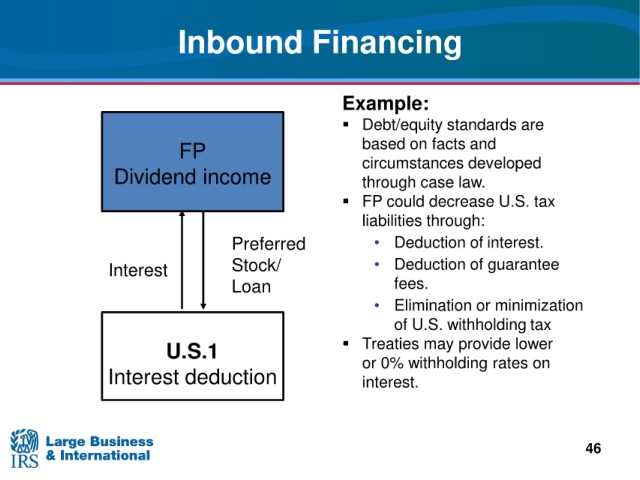

Inbound Financing

Example:

Debt/equity

standards are

and

FP based on facts

developed

circumstances

Dividend income through case law.

FP could decrease U.S. tax

liabilities through:

Preferred • Deduction of interest.

guarantee

Stock/ • Deduction of

Interest

Loan fees.

minimization

• Elimination or

of U.S. withholding tax

provide lower

U.S.1 Treaties may

or 0% withholding rates on

Interest deduction interest.

46