Page 69 - GTBank Annual Report 2020 eBook

P. 69

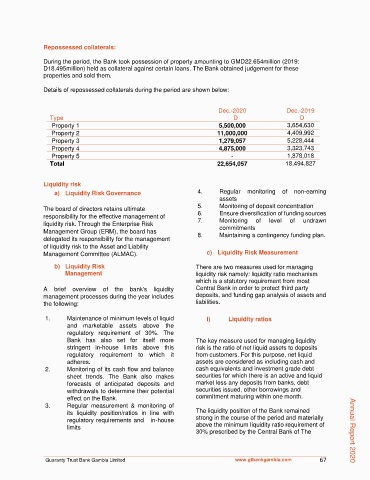

Repossessed collaterals:

During the period, the Bank took possession of property amounting to GMD22.654million (2019:

D18.495million) held as collateral against certain loans. The Bank obtained judgement for these

properties and sold them.

Details of repossessed collaterals during the period are shown below:

Dec.-2020 Dec.-2019

Type D

D

Property 1 5,500,000 3,654,630

Property 2 11,000,000 4,409,992

Property 3 1,279,057 5,228,444

Property 4 4,875,000 3,323,743

Property 5 - 1,878,018

Total 22,654,057 18,494,827

Liquidity risk

a) Liquidity Risk Governance 4. Regular monitoring of non-earning

assets

The board of directors retains ultimate 5. Monitoring of deposit concentration

responsibility for the effective management of 6. Ensure diversification of funding sources

liquidity risk. Through the Enterprise Risk 7. Monitoring of level of undrawn

commitments

Management Group (ERM), the board has 8. Maintaining a contingency funding plan.

delegated its responsibility for the management

of liquidity risk to the Asset and Liability

Management Committee (ALMAC). c) Liquidity Risk Measurement

b) Liquidity Risk There are two measures used for managing

Management liquidity risk namely: liquidity ratio mechanism

which is a statutory requirement from most

A brief overview of the bank's liquidity Central Bank in order to protect third party

management processes during the year includes deposits, and funding gap analysis of assets and

the following: liabilities.

1. Maintenance of minimum levels of liquid i) Liquidity ratios

and marketable assets above the

regulatory requirement of 30%. The

Bank has also set for itself more The key measure used for managing liquidity

stringent in-house limits above this risk is the ratio of net liquid assets to deposits

regulatory requirement to which it from customers. For this purpose, net liquid

adheres. assets are considered as including cash and

2. Monitoring of its cash flow and balance cash equivalents and investment grade debt

sheet trends. The Bank also makes securities for which there is an active and liquid

forecasts of anticipated deposits and market less any deposits from banks, debt

withdrawals to determine their potential securities issued, other borrowings and

effect on the Bank. commitment maturing within one month.

3. Regular measurement & monitoring of

its liquidity position/ratios in line with The liquidity position of the Bank remained

regulatory requirements and in-house strong in the course of the period and materially

limits above the minimum liquidity ratio requirement of

30% prescribed by the Central Bank of The Annual Report 2020

Guaranty Trust Bank Gambia Limited www.gtbankgambia.com 67