Page 39 - Managerial Accounting-MGT 145

P. 39

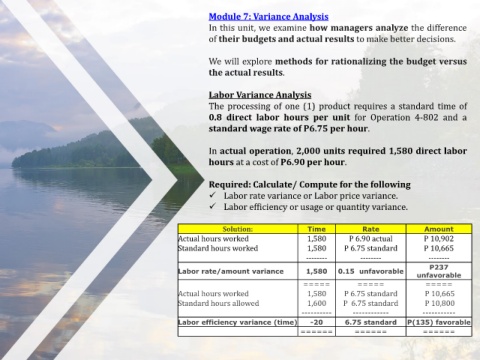

Module 7: Variance Analysis

In this unit, we examine how managers analyze the difference

of their budgets and actual results to make better decisions.

We will explore methods for rationalizing the budget versus

the actual results.

Labor Variance Analysis

The processing of one (1) product requires a standard time of

0.8 direct labor hours per unit for Operation 4-802 and a

standard wage rate of P6.75 per hour.

In actual operation, 2,000 units required 1,580 direct labor

hours at a cost of P6.90 per hour.

Required: Calculate/ Compute for the following

Labor rate variance or Labor price variance.

Labor efficiency or usage or quantity variance.

Solution: Time Rate Amount

Actual hours worked 1,580 P 6.90 actual P 10,902

Standard hours worked 1,580 P 6.75 standard P 10,665

-------- -------- --------

P237

Labor rate/amount variance 1,580 0.15 unfavorable

unfavorable

===== ===== =====

Actual hours worked 1,580 P 6.75 standard P 10,665

Standard hours allowed 1,600 P 6.75 standard P 10,800

---------- ------------ -----------

Labor efficiency variance (time) -20 6.75 standard P(135) favorable

====== ====== ======