Page 40 - Managerial Accounting-MGT 145

P. 40

Module 7: Variance Analysis

Module 7. REQUIREMENT

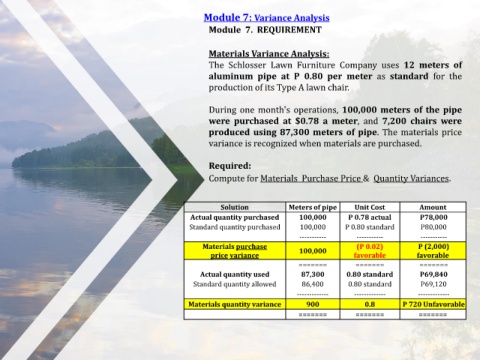

Materials Variance Analysis:

The Schlosser Lawn Furniture Company uses 12 meters of

aluminum pipe at P 0.80 per meter as standard for the

production of its Type A lawn chair.

During one month's operations, 100,000 meters of the pipe

were purchased at $0.78 a meter, and 7,200 chairs were

produced using 87,300 meters of pipe. The materials price

variance is recognized when materials are purchased.

Required:

Compute for Materials Purchase Price & Quantity Variances.

Solution Meters of pipe Unit Cost Amount

Actual quantity purchased 100,000 P 0.78 actual P78,000

Standard quantity purchased 100,000 P 0.80 standard P80,000

----------- ----------- -----------

Materials purchase 100,000 (P 0.02) P (2,000)

price variance favorable favorable

======= ======= =======

Actual quantity used 87,300 0.80 standard P69,840

Standard quantity allowed 86,400 0.80 standard P69,120

------------- ------------- -------------

Materials quantity variance 900 0.8 P 720 Unfavorable

======= ======= =======