Page 142 - ic92 actuarial

P. 142

The Insurance Times

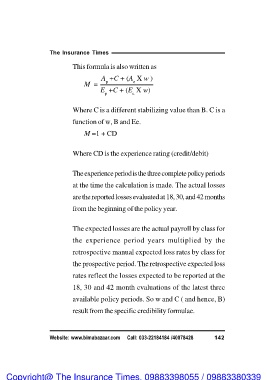

This formula is also written as

M = Ap +C + (Ae X w )

Ep +C + (Ee X w)

Where C is a different stabilizing value than B. C is a

function of w, B and Ee.

M =1 + CD

Where CD is the experience rating (credit/debit)

The experience period is the three complete policy periods

at the time the calculation is made. The actual losses

are the reported losses evaluated at 18, 30, and 42 months

from the beginning of the policy year.

The expected losses are the actual payroll by class for

the experience period years multiplied by the

retrospective manual expected loss rates by class for

the prospective period. The retrospective expected loss

rates reflect the losses expected to be reported at the

18, 30 and 42 month evaluations of the latest three

available policy periods. So w and C ( and hence, B)

result from the specific credibility formulae.

Website: www.bimabazaar.com Call: 033-22184184 /40078428 142

Copyright@ The Insurance Times. 09883398055 / 09883380339