Page 117 - IC26 LIFE INSURANCE FINANCE

P. 117

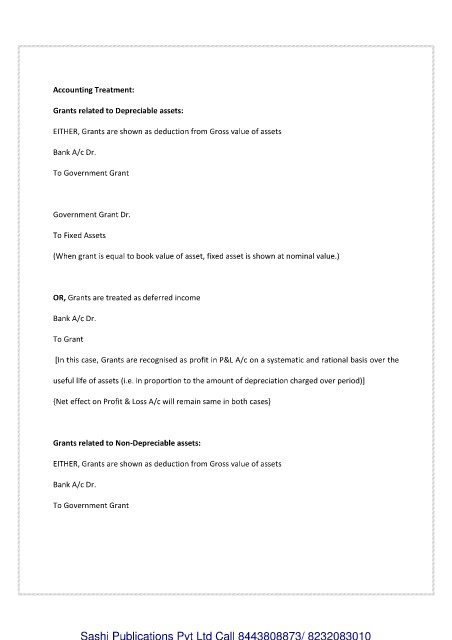

Accounting Treatment:

Grants related to Depreciable assets:

EITHER, Grants are shown as deduction from Gross value of assets

Bank A/c Dr.

To Government Grant

Government Grant Dr.

To Fixed Assets

(When grant is equal to book value of asset, fixed asset is shown at nominal value.)

OR, Grants are treated as deferred income

Bank A/c Dr.

To Grant

[In this case, Grants are recognised as profit in P&L A/c on a systematic and rational basis over the

useful life of assets (i.e. in proportion to the amount of depreciation charged over period)]

{Net effect on Profit & Loss A/c will remain same in both cases}

Grants related to Non-Depreciable assets:

EITHER, Grants are shown as deduction from Gross value of assets

Bank A/c Dr.

To Government Grant

Sashi Publications Pvt Ltd Call 8443808873/ 8232083010