Page 32 - Risk Management in current scenario

P. 32

company will have lower capital requirement as compare to poorly risk

managed company. Therefore solvency-II provides incentive to invest in

risk management.

Risk based capital is calculated using value at risk (VaR) methodology. This

is a statistical tool where VaR is calculated as maximum loss to the company

in a given time frame and within certain level of probability. This time frame

could be one day or one year or any other period as desired and probability

level could be 99% or 99.5% any level required for the purpose.

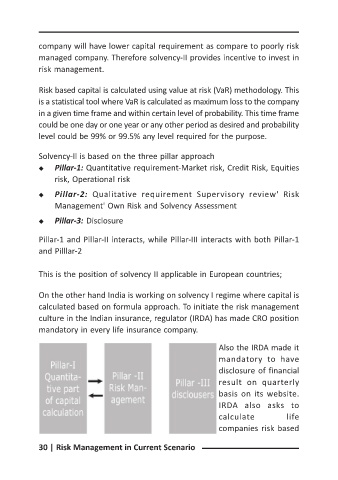

Solvency-Il is based on the three pillar approach

X Pillar-1: Quantitative requirement-Market risk, Credit Risk, Equities

risk, Operational risk

X Pillar-2: Qualitative requirement Supervisory review' Risk

Management' Own Risk and Solvency Assessment

X Pillar-3: Disclosure

Pillar-1 and Pillar-II interacts, while Pillar-III interacts with both Pillar-1

and Pilllar-2

This is the position of solvency II applicable in European countries;

On the other hand India is working on solvency I regime where capital is

calculated based on formula approach. To initiate the risk management

culture in the Indian insurance, regulator (IRDA) has made CRO position

mandatory in every life insurance company.

Also the IRDA made it

mandatory to have

disclosure of financial

result on quarterly

basis on its website.

IRDA also asks to

calculate life

companies risk based

30 | Risk Management in Current Scenario