Page 410 - SBR Integrated Workbook STUDENT S18-J19

P. 410

Chapter 25

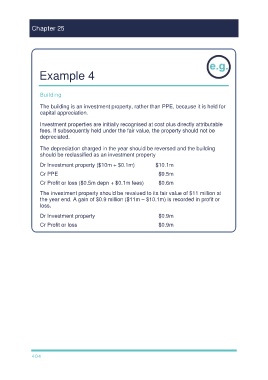

Example 4

Building

The building is an investment property, rather than PPE, because it is held for

capital appreciation.

Investment properties are initially recognised at cost plus directly attributable

fees. If subsequently held under the fair value, the property should not be

depreciated.

The depreciation charged in the year should be reversed and the building

should be reclassified as an investment property

Dr Investment property ($10m + $0.1m) $10.1m

Cr PPE $9.5m

Cr Profit or loss ($0.5m depn + $0.1m fees) $0.6m

The investment property should be revalued to its fair value of $11 million at

the year end. A gain of $0.9 million ($11m – $10.1m) is recorded in profit or

loss.

Dr Investment property $0.9m

Cr Profit or loss $0.9m

404