Page 342 - Microsoft Word - 00 CIMA F1 Prelims STUDENT 2018.docx

P. 342

Chapter 12

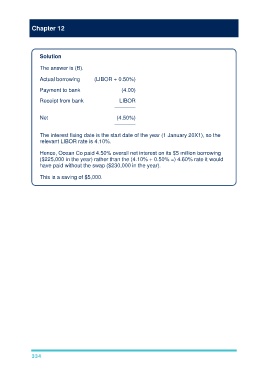

Solution

The answer is (B).

Actual borrowing (LIBOR + 0.50%)

Payment to bank (4.00)

Receipt from bank LIBOR

–––––––

Net (4.50%)

–––––––

The interest fixing date is the start date of the year (1 January 20X1), so the

relevant LIBOR rate is 4.10%.

Hence, Ocean Co paid 4.50% overall net interest on its $5 million borrowing

($225,000 in the year) rather than the (4.10% + 0.50% =) 4.60% rate it would

have paid without the swap ($230,000 in the year).

This is a saving of $5,000.

334