Page 166 - BA2 Integrated Workbook STUDENT 2018

P. 166

Chapter 9

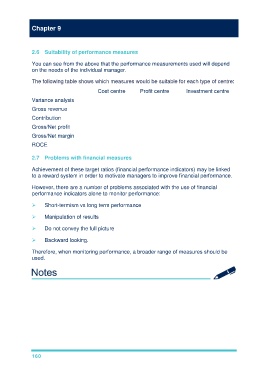

2.6 Suitability of performance measures

You can see from the above that the performance measurements used will depend

on the needs of the individual manager.

The following table shows which measures would be suitable for each type of centre:

Cost centre Profit centre Investment centre

Variance analysis

Gross revenue

Contribution

Gross/Net profit

Gross/Net margin

ROCE

2.7 Problems with financial measures

Achievement of these target ratios (financial performance indicators) may be linked

to a reward system in order to motivate managers to improve financial performance.

However, there are a number of problems associated with the use of financial

performance indicators alone to monitor performance:

Short-termism vs long term performance

Manipulation of results

Do not convey the full picture

Backward looking.

Therefore, when monitoring performance, a broader range of measures should be

used.

160