Page 91 - BA2 Integrated Workbook STUDENT 2018

P. 91

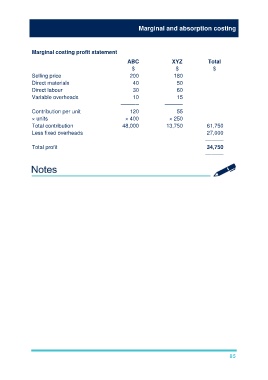

Marginal and absorption costing

Marginal costing profit statement

ABC XYZ Total

$ $ $

Selling price 200 180

Direct materials 40 50

Direct labour 30 60

Variable overheads 10 15

–––––– ––––––

Contribution per unit 120 55

× units × 400 × 250

Total contribution 48,000 13,750 61,750

Less fixed overheads 27,000

––––––

Total profit 34,750

––––––

85