Page 494 - F2 - MA Integrated Workbook STUDENT 2018-19

P. 494

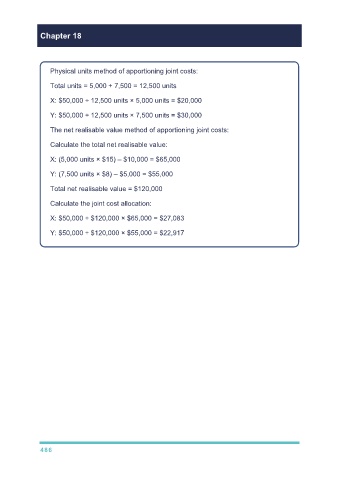

Chapter 18

Physical units method of apportioning joint costs:

Total units = 5,000 + 7,500 = 12,500 units

X: $50,000 ÷ 12,500 units × 5,000 units = $20,000

Y: $50,000 ÷ 12,500 units × 7,500 units = $30,000

The net realisable value method of apportioning joint costs:

Calculate the total net realisable value:

X: (5,000 units × $15) – $10,000 = $65,000

Y: (7,500 units × $8) – $5,000 = $55,000

Total net realisable value = $120,000

Calculate the joint cost allocation:

X: $50,000 ÷ $120,000 × $65,000 = $27,083

Y: $50,000 ÷ $120,000 × $55,000 = $22,917

486