Page 9 - FINAL CFA II SLIDES JUNE 2019 DAY 8

P. 9

LOS 31.b: Calculate and interpret a justified price multiple. READING 31: MARKET-BASED VALUATION: PRICE AND

LOS 31.c: Describe rationales for and possible drawbacks ENTERPRISE VALUE MULTIPLES

to using alternative price multiples and dividend yield in

valuation. MODULE 31.4: EV AND OTHER ASPECTS

LOS 31.d: Calculate and interpret alternative price

multiples and dividend yield.

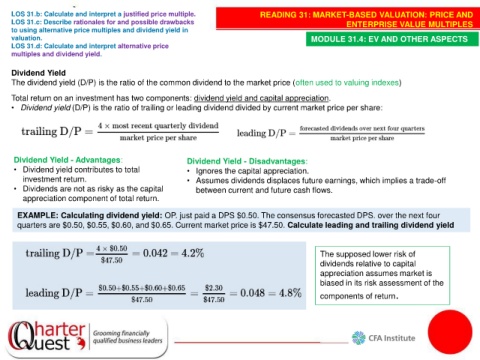

Dividend Yield

The dividend yield (D/P) is the ratio of the common dividend to the market price (often used to valuing indexes)

Total return on an investment has two components: dividend yield and capital appreciation.

• Dividend yield (D/P) is the ratio of trailing or leading dividend divided by current market price per share:

Dividend Yield - Advantages: Dividend Yield - Disadvantages:

• Dividend yield contributes to total • Ignores the capital appreciation.

investment return. • Assumes dividends displaces future earnings, which implies a trade-off

• Dividends are not as risky as the capital between current and future cash flows.

appreciation component of total return.

EXAMPLE: Calculating dividend yield: OP. just paid a DPS $0.50. The consensus forecasted DPS. over the next four

quarters are $0.50, $0.55, $0.60, and $0.65. Current market price is $47.50. Calculate leading and trailing dividend yield

The supposed lower risk of

dividends relative to capital

appreciation assumes market is

biased in its risk assessment of the

components of return.