Page 25 - P6 Slide Taxation - Lecture Day 4

P. 25

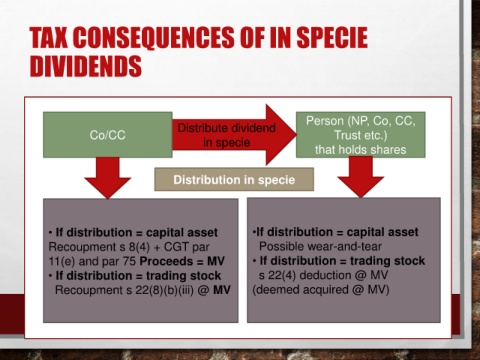

TAX CONSEQUENCES OF IN SPECIE

DIVIDENDS

Person (NP, Co, CC,

Distribute dividend

Co/CC Trust etc.)

in specie

that holds shares

Distribution in specie

• If distribution = capital asset •If distribution = capital asset

Recoupment s 8(4) + CGT par Possible wear-and-tear

11(e) and par 75 Proceeds = MV • If distribution = trading stock

• If distribution = trading stock s 22(4) deduction @ MV

Recoupment s 22(8)(b)(iii) @ MV (deemed acquired @ MV)