Page 10 - PowerPoint Presentation

P. 10

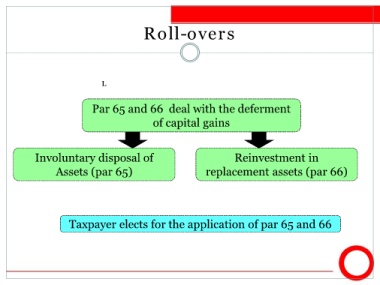

Roll-overs

L

Par 65 and 66 deal with the deferment

of capital gains

Involuntary disposal of Reinvestment in

Assets (par 65) replacement assets (par 66)

Taxpayer elects for the application of par 65 and 66