Page 14 - P6 Slide Taxation - Lecture Day 6 - Groups, Interest And Practice Questions

P. 14

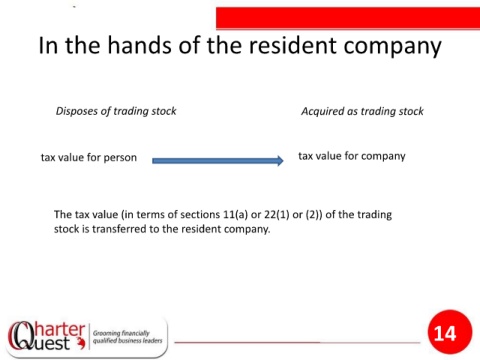

In the hands of the resident company

Disposes of trading stock Acquired as trading stock

tax value for person tax value for company

The tax value (in terms of sections 11(a) or 22(1) or (2)) of the trading

stock is transferred to the resident company.

14