Page 442 - Microsoft Word - 00 BA3 IW Prelims STUDENT.docx

P. 442

Fundamentals of financial accounting

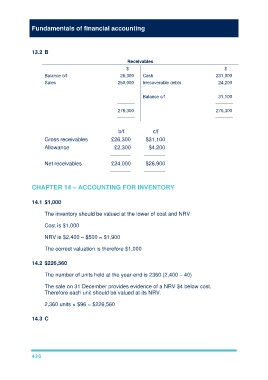

13.2 B

Receivables

$ $

Balance b/f 26,300 Cash 231,000

Sales 250,000 Irrecoverable debts 24,200

Balance c/f 31,100

––––––– –––––––

276,300 276,300

––––––– –––––––

b/f c/f

Gross receivables £26,300 $31,100

Allowance £2,300 $4,200

––––––– –––––––

Net receivables £24,000 $26,900

––––––– –––––––

CHAPTER 14 – ACCOUNTING FOR INVENTORY

14.1 $1,000

The inventory should be valued at the lower of cost and NRV

Cost is $1,000

NRV is $2,400 – $500 = $1,900

The correct valuation is therefore $1,000

14.2 $226,560

The number of units held at the year-end is 2360 (2,400 – 40)

The sale on 31 December provides evidence of a NRV $4 below cost.

Therefore each unit should be valued at its NRV.

2,360 units × $96 = $226,560

14.3 C

436