Page 6 - 01 Cotton SA May 2013

P. 6

Markverslag • Market Repor t

Cotton MarKet rePort as at 2 MaY 2013

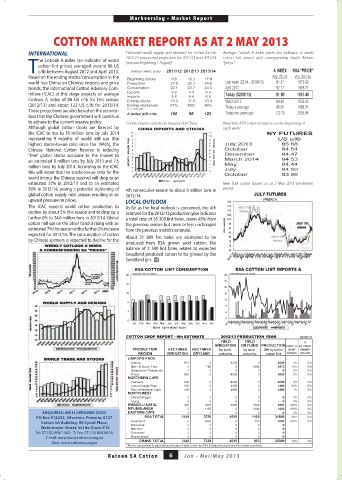

iNterNatioNal Estimated world supply and demand for cotton for the Average Cotlook A index prices (an indicator of world

he Cotlook A index (an indicator of world 2011/12 season and projections for 2012/13 and 2013/14 cotton lint prices) and corresponding South African

“prices”:

(seasons beginning 1 August):

cotton lint prices) averaged around 86 US

Tc/lb between August 2012 and April 2013.

Based on the ending stocks/consumption in the

world less China; on Chinese imports and price

trends, the International Cotton Advisory Com-

mittee (ICAC) at this stage projects an average

Cotlook A index of 88 US c/lb for this season

(2012/13) and about 122 US c/lb for 2013/14.

These projections are also based on the assump-

tion that the Chinese government will continue

to adhere to the current reserve policy. Cotton imports and stocks situation for China: New York JULY cotton futures as at the beginning of

Although global cotton stocks are forecast by each week:

the ICAC to rise to 18 million tons by July 2014

representing 9 months of world mill use (the

highest stocks-to-use ratio since the 1940’s), the

Chinese National Cotton Reserve is reducing

“free” global stocks available to the market to

an estimated 9 million tons by July 2013 and 7.5

million tons by July 2014. According to the ICAC

this will mean that the stocks-to-use ratio for the

world (minus the Chinese reserve) will drop to an

estimated 37% in 2012/13 and to an estimated New York cotton futures as at 2 May 2013 (settlement

30% in 2013/14, posing a potential tightening of 4th consecutive season to about 8 million tons in prices):

global cotton supply next season resulting in an 2013/14.

upward pressure on prices. local outlooK

The ICAC expects world cotton production to As far as the local outlook is concerned, the 4th

decline by about 5% this season and to drop by a estimate for the 2012/13 production year indicates

further 6% to 24.6 million tons in 2013/14. Global a total crop of 35 309 lint bales, down 45% from

cotton mill use on the other hand is rising with an the previous season but more or less unchanged

estimated 7% this season with a further 2% increase from the previous month’s estimate.

expected for 2013/14. The consumption of cotton About 31 809 lint bales are estimated to be

by Chinese spinners is expected to decline for the

produced from RSA grown seed cotton. The

balance of 3 500 lint bales relates to expected

Swaziland produced cotton to be ginned by the

Swaziland gin.

ENQUIRIES: MR H J BRUWER (CEO)

PO Box 912232, Silverton, Pretoria, 0127

Cotton SA Building, 90 Cycad Place,

Watermeyer Street, Val de Grace X10

Tel: 27 (12) 804 1462 - 7; Fax: 27 (12) 804 8616;

E-mail: enquiries@cottonsa.org.za

Web: www.cottonsa.org.za

Katoen sa Cotton 6 Jan - Mei/May 2013