Page 13 - Parkside Gasification & Pellet Plant Report 081117_Neat

P. 13

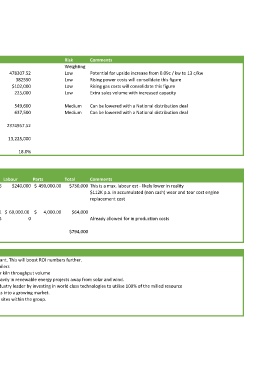

Comments Potential for upside increase from 0.09c / kw to 13 c/kw Rising power costs will consolidate this figure Rising gas costs will consolidate this figure Extra sales volume with increased capacity Can be lowered with a National distribution deal Can be lowered with a National distribution deal Comments This is a max. labour est ‐ likely lower in reality $112K p.a. in accumulated (non cash) wear and tear cost engine replacement cost Already allowed for in production costs

Weighting Medium Medium $730,000 $64,000 $794,000

Risk Low Low Low Low Total

490,000.00 4,000.00 Parkside has the opportunity to become an industry leader by investing in world class technologies to utilise 100% of the milled resource

Parts $ $ 0

478307.52 382550 $102,000 225,000 549,600 637,500 2374957.52 13,225,000 18.0% Labour $240,000 60,000.00 CEFC have recently been directed to invest heavily in renewable energy projects away from solar and wind.

6 $ 1 1.5 Obtain ARENA co‐funding for on site energy plant. This will boost ROI numbers further.

No. workers Negotiate a stronger FIT energy price with retailers Additional profit from extra sales due to higher kiln throughput volume Will become a very low cost producer of pellets into a growing market. The technology solution is repeatable at other sites within the group.

PARKSIDE GROUP ‐ Investment Returns

Revenue streams Electrical income external Electrical income internal Gas savings Inc. kiln drying capacity benefit $25 / m3 x 9,000m3 p.a.) Pellet sales profit15kg bags Briquette sales profit Total free cash generated Investment amount ROI OpEx Costs ‐ annual Gasifiers: 7 units RUF / FLR 1000 CPM press Total OpEx Opportunities 1. 2. 3. 4. 5. 6. 7.

MW hrs 8085 1677.472 6407.528 1093 350 382550 5314.528 478307.5 860857.5 8659 189891 52,747 52.7 $102,000 $408,000 549,600 637,500

Projected savings after CapEx Stage 1 energy generation less extra energy consumption Surplus energy generated Current energy consumed from grid Current energy cost / MW Total current energy cost Surplus energy exported Revenue at $90 / Mw Total electrical energy savings Gas for kiln total lt. Total energy Mj Equivalent kWTh Equivalent MwTh Current gas cost 50 degrees drying temp Projected gas cost 70 degrees drying temp Profit from pellets 3000T / 15kg bags x $2.75/ bag profit Profit from briquettes 1700T / 8kg bags x $3/ bag profit