Page 165 - VIRANSH COACHING CLASSES

P. 165

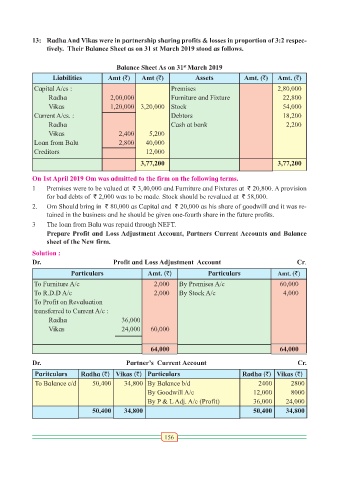

13: Radha And Vikas were in partnership sharing profits & losses in proportion of 3:2 respec-

tively. Their Balance Sheet as on 31 st March 2019 stood as follows.

st

Balance Sheet As on 31 March 2019

Liabilities Amt (`) Amt (`) Assets Amt. (`) Amt. (`)

Capital A/cs : Premises 2,80,000

Radha 2,00,000 Furniture and Fixture 22,800

Vikas 1,20,000 3,20,000 Stock 54,000

Current A/cs. : Debtors 18,200

Radha Cash at bank 2,200

Vikas 2,400 5,200

Loan from Balu 2,800 40,000

Creditors 12,000

3,77,200 3,77,200

On 1st April 2019 Om was admitted to the firm on the following terms.

1 Premises were to be valued at ` 3,40,000 and Furniture and Fixtures at ` 20,800. A provision

for bad debts of ` 2,000 was to be made. Stock should be revalued at ` 58,000.

2. Om Should bring in ` 80,000 as Capital and ` 20,000 as his share of goodwill and it was re-

tained in the business and he should be given one-fourth share in the future profits.

3 The loan from Balu was repaid through NEFT.

Prepare Profit and Loss Adjustment Account, Partners Current Accounts and Balance

sheet of the New firm.

Solution :

Dr. Profit and Loss Adjustment Account Cr.

Particulars Amt. (`) Particulars Amt. (`)

To Furniture A/c 2,000 By Premises A/c 60,000

To R.D.D A/c 2,000 By Stock A/c 4,000

To Profit on Revaluation

transferred to Current A/c :

Radha 36,000

Vikas 24,000 60,000

64,000 64,000

Dr. Partner’s Current Account Cr.

Paritculars Radha (`) Vikas (`) Particulars Radha (`) Vikas (`)

To Balance c/d 50,400 34,800 By Balance b/d 2400 2800

By Goodwill A/c 12,000 8000

By P & L Adj. A/c (Profit) 36,000 24,000

50,400 34,800 50,400 34,800

156