Page 306 - VIRANSH COACHING CLASSES

P. 306

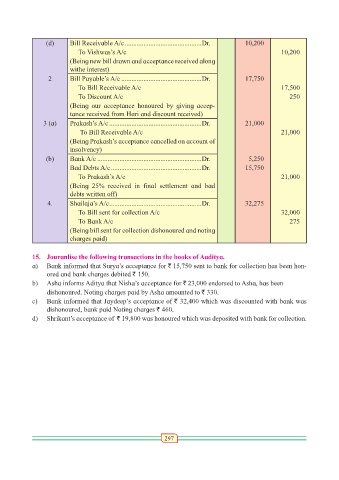

(d) Bill Receivable A/c .............................................Dr. 10,200

To Vishwas’s A/c 10,200

(Being new bill drawn and acceptance received along

withe interest)

2 Bill Payable’s A/c ...............................................Dr. 17,750

To Bill Receivable A/c 17,500

To Discount A/c 250

(Being our acceptance honoured by giving accep-

tance received from Hari and discount received)

3 (a) Prakash’s A/c ......................................................Dr. 21,000

To Bill Receivable A/c 21,000

(Being Prakash’s acceptance cancelled on account of

insolvency)

(b) Bank A/c .............................................................Dr. 5,250

Bad Debts A/c .....................................................Dr. 15,750

To Prakash’s A/c 21,000

(Being 25% received in final settlement and bad

debts written off)

4. Shailaja’s A/c ......................................................Dr. 32,275

To Bill sent for collection A/c 32,000

To Bank A/c 275

(Being bill sent for collection dishonoured and noting

charges paid)

15. Jouranlise the following transactions in the books of Aaditya.

a) Bank informed that Surya’s acceptance for ` 15,750 sent to bank for collection has been hon-

ored and bank charges debited ` 150.

b) Asha informs Aditya that Nisha’s acceptance for ` 23,000 endorsed to Asha, has been

dishonoured. Noting charges paid by Asha amounted to ` 330.

c) Bank informed that Jaydeep’s acceptance of ` 32,400 which was discounted with bank was

dishonoured, bank paid Noting charges ` 460.

d) Shrikant’s acceptance of ` 19,800 was honoured which was deposited with bank for collection.

297