Page 301 - VIRANSH COACHING CLASSES

P. 301

In the books of Navin

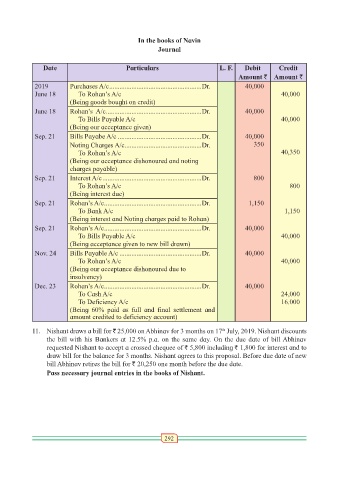

Journal

Date Particulars L. F. Debit Credit

Amount ` Amount `

2019 Purchases A/c ......................................................Dr. 40,000

June 18 To Rohan’s A/c 40,000

(Being goods bought on credit)

June 18 Rohan’s A/c. .......................................................Dr. 40,000

To Bills Payable A/c 40,000

(Being our acceptance given)

Sep. 21 Bills Payabe A/c .................................................Dr. 40,000

Noting Charges A/c .............................................Dr. 350

To Rohan’s A/c 40,350

(Being our acceptance dishonoured and noting

charges payable)

Sep. 21 Interest A/c ..........................................................Dr. 800

To Rohan’s A/c 800

(Being interest due)

Sep. 21 Rohan’s A/c .........................................................Dr. 1,150

To Bank A/c 1,150

(Being interest and Noting charges paid to Rohan)

Sep. 21 Rohan’s A/c .........................................................Dr. 40,000

To Bills Payable A/c 40,000

(Being acceptance given to new bill drawn)

Nov. 24 Bills Payable A/c ................................................Dr. 40,000

To Rohan’s A/c 40,000

(Being our acceptance dishonoured due to

insolvency)

Dec. 23 Rohan’s A/c .........................................................Dr. 40,000

To Cash A/c 24,000

To Deficiency A/c 16.000

(Being 60% paid as full and final settlement and

amount credited to deficiency account)

th

11. Nishant draws a bill for ` 25,000 on Abhinav for 3 months on 17 July, 2019. Nishant discounts

the bill with his Bankers at 12.5% p.a. on the same day. On the due date of bill Abhinav

requested Nishant to accept a crossed chequee of ` 5,800 including ` 1,800 for interest and to

draw bill for the balance for 3 months. Nishant agrees to this proposal. Before due date of new

bill Abhinav retires the bill for ` 20,250 one month before the due date.

Pass necessary journal entries in the books of Nishant.

292