Page 303 - VIRANSH COACHING CLASSES

P. 303

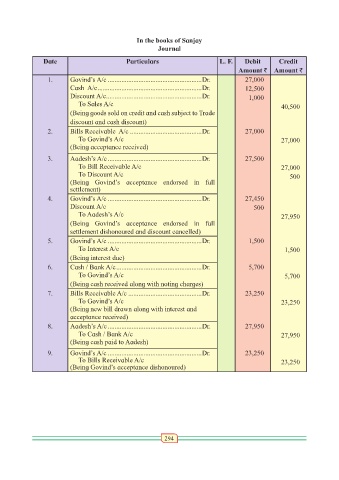

In the books of Sanjay

Journal

Date Particulars L. F. Debit Credit

Amount ` Amount `

1. Govind’s A/c .......................................................Dr. 27,000

Cash A/c .............................................................Dr. 12,500

Discount A/c ........................................................Dr. 1,000

To Sales A/c 40,500

(Being goods sold on credit and cash subject to Trade

discount and cash discount)

2. Bills Receivable A/c ..........................................Dr. 27,000

To Govind’s A/c 27,000

(Being acceptance received)

3. Aadesh’s A/c .......................................................Dr. 27,500

To Bill Receivable A/c 27,000

To Discount A/c 500

(Being Govind’s acceptance endorsed in full

settlement)

4. Govind’s A/c .......................................................Dr. 27,450

Discount A/c 500

To Aadesh’s A/c 27,950

(Being Govind’s acceptance endorsed in full

settlement dishonoured and discount cancelled)

5. Govind’s A/c .......................................................Dr. 1,500

To Interest A/c 1,500

(Being interest due)

6. Cash / Bank A/c ..................................................Dr. 5,700

To Govind’s A/c 5,700

(Being cash received along with noting charges)

7. Bills Receivable A/c ...........................................Dr. 23,250

To Govind’s A/c 23,250

(Being new bill drawn along with interest and

acceptance received)

8. Aadesh’s A/c .......................................................Dr. 27,950

To Cash / Bank A/c 27,950

(Being cash paid to Aadesh)

9. Govind’s A/c .......................................................Dr. 23,250

To Bills Receivable A/c 23,250

(Being Govind’s acceptance dishonoured)

294