Page 297 - VIRANSH COACHING CLASSES

P. 297

7. On 15 September, 2019 Kunal purchased goods from Kishorilal for ` 38,000 and Kunal gave

th

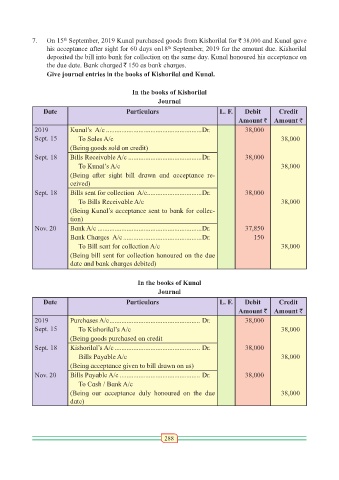

his acceptance after sight for 60 days on18 September, 2019 for the amount due. Kishorilal

th

deposited the bill into bank for collection on the same day. Kunal honoured his acceptance on

the due date. Bank charged ` 150 as bank charges.

Give journal entries in the books of Kishorilal and Kunal.

In the books of Kishorilal

Journal

Date Particulars L. F. Debit Credit

Amount ` Amount `

2019 Kunal’s A/c ........................................................Dr. 38,000

Sept. 15 To Sales A/c 38,000

(Being goods sold on credit)

Sept. 18 Bills Receivable A/c ...........................................Dr. 38,000

To Kunal’s A/c 38,000

(Being after sight bill drawn and acceptance re-

ceived)

Sept. 18 Bills sent for collection A/c ................................Dr. 38,000

To Bills Receivable A/c 38,000

(Being Kunal’s acceptance sent to bank for collec-

tion)

Nov. 20 Bank A/c .............................................................Dr. 37,850

Bank Charges A/c ..............................................Dr. 150

To Bill sent for collection A/c 38,000

(Being bill sent for collection honoured on the due

date and bank charges debited)

In the books of Kunal

Journal

Date Particulars L. F. Debit Credit

Amount ` Amount `

2019 Purchases A/c ..................................................... Dr. 38,000

Sept. 15 To Kishorilal’s A/c 38,000

(Being goods purchased on credit

Sept. 18 Kishorilal’s A/c .................................................. Dr. 38,000

Bills Payable A/c 38,000

(Being acceptance given to bill drawn on us)

Nov. 20 Bills Payable A/c ............................................... Dr. 38,000

To Cash / Bank A/c

(Being our acceptance duly honoured on the due 38,000

date)

288