Page 335 - VIRANSH COACHING CLASSES

P. 335

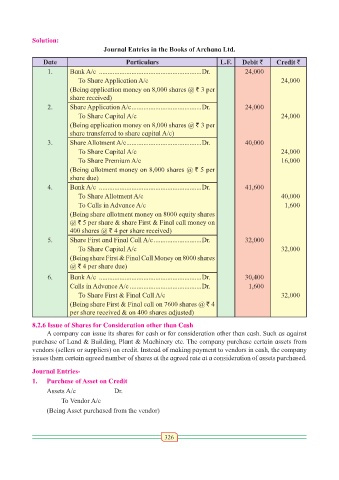

Solution:

Journal Entries in the Books of Archana Ltd.

Date Particulars L.F. Debit ` Credit `

1. Bank A/c ............................................................Dr. 24,000

To Share Application A/c 24,000

(Being application money on 8,000 shares @ ` 3 per

share received)

2. Share Application A/c .........................................Dr. 24,000

To Share Capital A/c 24,000

(Being application money on 8,000 shares @ ` 3 per

share transferred to share capital A/c)

3. Share Allotment A/c ............................................Dr. 40,000

To Share Capital A/c 24,000

To Share Premium A/c 16,000

(Being allotment money on 8,000 shares @ ` 5 per

share due)

4. Bank A/c ............................................................Dr. 41,600

To Share Allotment A/c 40,000

To Calls in Advance A/c 1,600

(Being share allotment money on 8000 equity shares

@ ` 5 per share & share First & Final call money on

400 shares @ ` 4 per share received)

5. Share First and Final Call A/c ............................Dr. 32,000

To Share Capital A/c 32,000

(Being share First & Final Call Money on 8000 shares

@ ` 4 per share due)

6. Bank A/c ............................................................Dr. 30,400

Calls in Advance A/c ..........................................Dr. 1,600

To Share First & Final Call A/c 32,000

(Being share First & Final call on 7600 shares @ ` 4

per share received & on 400 shares adjusted)

8.2.6 Issue of Shares for Consideration other than Cash

A company can issue its shares for cash or for consideration other than cash. Such as against

purchase of Land & Building, Plant & Machinery etc. The company purchase certain assets from

vendors (sellers or suppliers) on credit. Instead of making payment to vendors in cash, the company

issues them certain agreed number of shares at the agreed rate at a consideration of assets purchased.

Journal Entries-

1. Purchase of Asset on Credit

Assets A/c Dr.

To Vendor A/c

(Being Asset purchased from the vendor)

326