Page 29 - NYMets_2018_Benefits_Guide

P. 29

BACK TO

HOME

PLATE

at-bat: 401(k) Retirement Savings

For many of us, retirement is probably a long way off; for others, it may be in the near future. Whatever life stage you are in, it is

never too soon (or too late!) to start saving for the future. Sterling Mets, LP offers you a convenient way to save by providing you

with a 401(k) Retirement Savings Plan through Fidelity.

The earlier you begin contributing and the more you can contribute...your account will grow over time. Building your nest egg now

means you will have money at retirement to enjoy life.

The chart below is a brief summary of the plan features. For more information and plan details, refer to the Fidelity materials.

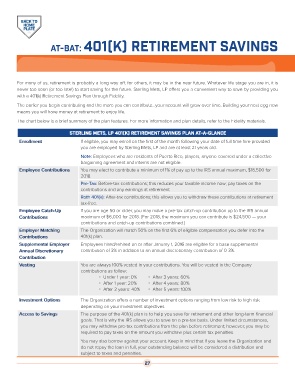

Sterling Mets, LP 401(k) Retirement Savings Plan At-a-Glance

Enrollment If eligible, you may enroll on the first of the month following your date of full time hire provided

you are employed by Sterling Mets, LP and are at least 21 years old.

Note: Employees who are residents of Puerto Rico, players, anyone covered under a collective-

bargaining agreement and interns are not eligible.

Employee Contributions You may elect to contribute a minimum of 1% of pay up to the IRS annual maximum, $18,500 for

2018.

Pre-Tax: Before-tax contributions; this reduces your taxable income now; pay taxes on the

contributions and any earnings at retirement

Roth 401(k): After-tax contributions; this allows you to withdraw these contributions at retirement

tax-free.

Employee Catch-Up If you are age 50 or older, you may make a pre-tax catch-up contribution up to the IRS annual

Contributions maximum of $6,000 for 2018. (For 2018, the maximum you can contribute is $24,500 — your

contributions and catch-up contributions combined.)

Employer Matching The Organization will match 50% on the first 6% of eligible compensation you defer into the

Contributions 401(k) plan.

Supplemental Employer Employees hired/rehired on or after January 1, 2016 are eligible for a base supplemental

Annual Discretionary contribution of 3% in addition to an annual discretionary contribution of 0-3%.

Contribution

Vesting You are always 100% vested in your contributions. You will be vested in the Company

contributions as follow:

Under 1 year: 0% After 3 years: 60%

After 1 year: 20% After 4 years: 80%

After 2 years: 40% After 5 years: 100%

Investment Options The Organization offers a number of investment options ranging from low risk to high risk

depending on your investment objectives.

Access to Savings The purpose of the 401(k) plan is to help you save for retirement and other long-term financial

goals. That is why the IRS allows you to save on a pre-tax basis. Under limited circumstances,

you may withdraw pre-tax contributions from the plan before retirement; however, you may be

required to pay taxes on the amount you withdraw plus certain tax penalties.

You may also borrow against your account. Keep in mind that if you leave the Organization and

do not repay the loan in full, your outstanding balance will be considered a distribution and

subject to taxes and penalties.

27