Page 161 - JoFA_2022

P. 161

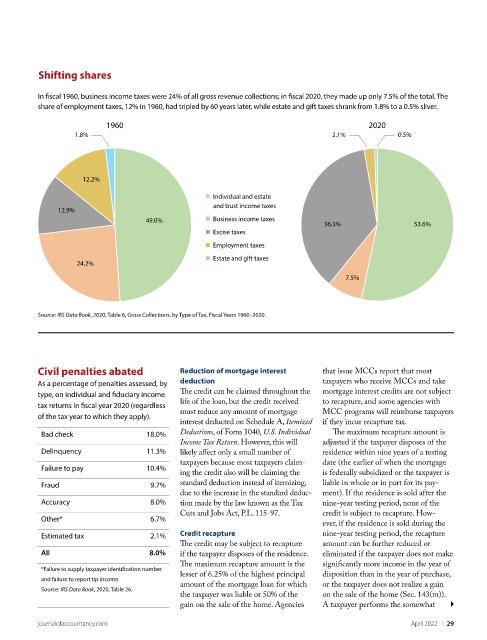

Shifting shares

In fiscal 1960, business income taxes were 24% of all gross revenue collections; in fiscal 2020, they made up only 7.5% of the total. The

share of employment taxes, 12% in 1960, had tripled by 60 years later, while estate and gift taxes shrank from 1.8% to a 0.5% sliver.

1960 2020

1.8% 2.1% 0.5%

12.2%

Individual and estate

and trust income taxes

12.9%

49.0% Business income taxes

36.3% 53.6%

Excise taxes

Employment taxes

Estate and gift taxes

24.2%

7.5%

Source: IRS Data Book, 2020, Table 6, Gross Collections, by Type of Tax, Fiscal Years 1960–2020.

Civil penalties abated Reduction of mortgage interest that issue MCCs report that most

As a percentage of penalties assessed, by deduction taxpayers who receive MCCs and take

type, on individual and fiduciary income The credit can be claimed throughout the mortgage interest credits are not subject

tax returns in fiscal year 2020 (regardless life of the loan, but the credit received to recapture, and some agencies with

of the tax year to which they apply). must reduce any amount of mortgage MCC programs will reimburse taxpayers

interest deducted on Schedule A, Itemized if they incur recapture tax.

Bad check 18.0% Deductions, of Form 1040, U.S. Individual The maximum recapture amount is

Income Tax Return. However, this will adjusted if the taxpayer disposes of the

Delinquency 11.3% likely affect only a small number of residence within nine years of a testing

taxpayers because most taxpayers claim- date (the earlier of when the mortgage

Failure to pay 10.4%

ing the credit also will be claiming the is federally subsidized or the taxpayer is

Fraud 9.7% standard deduction instead of itemizing, liable in whole or in part for its pay-

due to the increase in the standard deduc- ment). If the residence is sold after the

Accuracy 8.0% tion made by the law known as the Tax nine-year testing period, none of the

Cuts and Jobs Act, P.L. 115-97. credit is subject to recapture. How-

Other* 6.7%

ever, if the residence is sold during the

Estimated tax 2.1% Credit recapture nine-year testing period, the recapture

The credit may be subject to recapture amount can be further reduced or

All 8.0% if the taxpayer disposes of the residence. eliminated if the taxpayer does not make

The maximum recapture amount is the significantly more income in the year of

*Failure to supply taxpayer identification number

lesser of 6.25% of the highest principal disposition than in the year of purchase,

and failure to report tip income.

amount of the mortgage loan for which or the taxpayer does not realize a gain

Source: IRS Data Book, 2020, Table 26.

the taxpayer was liable or 50% of the on the sale of the home (Sec. 143(m)).

gain on the sale of the home. Agencies A taxpayer performs the somewhat

journalofaccountancy.com April 2022 | 29