Page 205 - JoFA_2022

P. 205

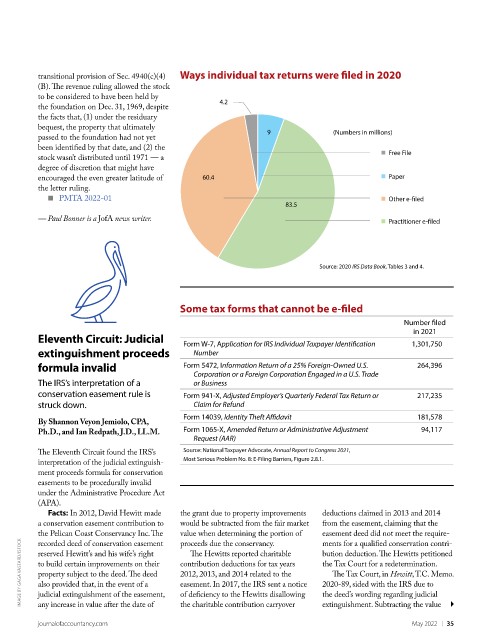

Ways individual tax returns were filed in 2020

transitional provision of Sec. 4940(c)(4)

(B). The revenue ruling allowed the stock

to be considered to have been held by

4.2

the foundation on Dec. 31, 1969, despite

the facts that, (1) under the residuary

bequest, the property that ultimately

9 (Numbers in millions)

passed to the foundation had not yet

been identified by that date, and (2) the

Free File

stock wasn’t distributed until 1971 — a

degree of discretion that might have

encouraged the even greater latitude of 60.4 Paper

the letter ruling.

■ PMTA 2022-01 Other e-filed

83.5

— Paul Bonner is a JofA news writer. Practitioner e-filed

Source: 2020 IRS Data Book, Tables 3 and 4.

Some tax forms that cannot be e-filed

Number filed

in 2021

Eleventh Circuit: Judicial For m W-7, Application for IRS Individual Taxpayer Identification 1,301,750

extinguishment proceeds Number

formula invalid For m 5472, Information Return of a 25% Foreign-Owned U.S. 264,396

Corporation or a Foreign Corporation Engaged in a U.S. Trade

The IRS’s interpretation of a or Business

conservation easement rule is For m 941-X, Adjusted Employer’s Quarterly Federal Tax Return or 217,235

struck down. Claim for Refund

Form 14039, Identity Theft Affidavit 181,578

By Shannon Veyon Jemiolo, CPA,

For m 1065-X, Amended Return or Administrative Adjustment 94,117

Ph.D., and Ian Redpath, J.D., LL.M.

Request (AAR)

Source: National Taxpayer Advocate, Annual Report to Congress 2021,

The Eleventh Circuit found the IRS’s

Most Serious Problem No. 8: E-Filing Barriers, Figure 2.8.1.

interpretation of the judicial extinguish-

ment proceeds formula for conservation

easements to be procedurally invalid

under the Administrative Procedure Act

(APA).

Facts: In 2012, David Hewitt made the grant due to property improvements deductions claimed in 2013 and 2014

a conservation easement contribution to would be subtracted from the fair market from the easement, claiming that the

the Pelican Coast Conservancy Inc. The value when determining the portion of easement deed did not meet the require-

IMAGE BY GAGA VASTARD/ISTOCK reserved Hewitt’s and his wife’s right contribution deductions for tax years bution deduction. The Hewitts petitioned

recorded deed of conservation easement

proceeds due the conservancy.

ments for a qualified conservation contri-

The Hewitts reported charitable

to build certain improvements on their

the Tax Court for a redetermination.

The Tax Court, in Hewitt, T.C. Memo.

2012, 2013, and 2014 related to the

property subject to the deed. The deed

2020-89, sided with the IRS due to

also provided that, in the event of a

easement. In 2017, the IRS sent a notice

judicial extinguishment of the easement,

of deficiency to the Hewitts disallowing

the deed’s wording regarding judicial

any increase in value after the date of

May 2022 | 35

journalofaccountancy.com the charitable contribution carryover extinguishment. Subtracting the value