Page 371 - JoFA_2022

P. 371

FRAUD / AUDITING

The first-two digits of the population of was then “exploded” out into a half-million journal

journal entries entries per year, all below the auditors’ $5,000

testing threshold.

I ran a simulation to show that Benford’s

Law-based testing could have detected a fraud

scheme executed using below-the-testing-threshold

dollar amounts, and I show the results below. In

a real-world audit, the audit population would be

all the journal entries posted from the date of the

trial balance at the end of the prior year to the date

of the trial balance in the current year. The testing

objective would be to identify journal entries made

in amounts below the testing threshold ($5,000 in

HealthSouth’s case) that materially changed the

ledger account balances and created a fraudulent set

of financial statements.

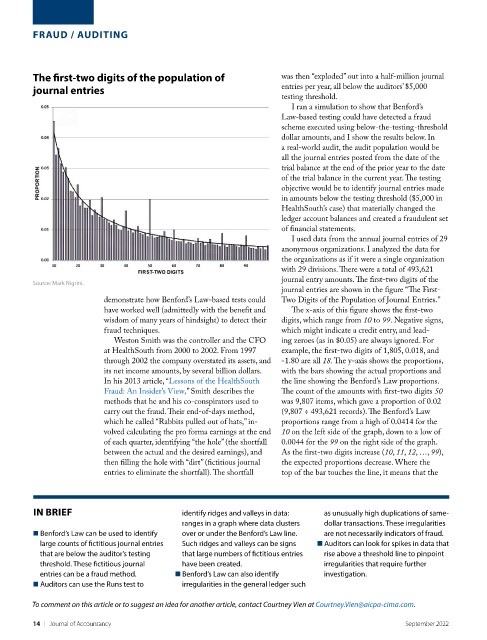

I used data from the annual journal entries of 29

anonymous organizations. I analyzed the data for

the organizations as if it were a single organization

with 29 divisions. There were a total of 493,621

Source: Mark Nigrini. journal entry amounts. The first-two digits of the

journal entries are shown in the figure “The First-

demonstrate how Benford’s Law-based tests could Two Digits of the Population of Journal Entries.”

have worked well (admittedly with the benefit and The x-axis of this figure shows the first-two

wisdom of many years of hindsight) to detect their digits, which range from 10 to 99. Negative signs,

fraud techniques. which might indicate a credit entry, and lead-

Weston Smith was the controller and the CFO ing zeroes (as in $0.05) are always ignored. For

at HealthSouth from 2000 to 2002. From 1997 example, the first-two digits of 1,805, 0.018, and

through 2002 the company overstated its assets, and -1.80 are all 18. The y-axis shows the proportions,

its net income amounts, by several billion dollars. with the bars showing the actual proportions and

In his 2013 article, “Lessons of the HealthSouth the line showing the Benford’s Law proportions.

Fraud: An Insider’s View,” Smith describes the The count of the amounts with first-two digits 50

methods that he and his co-conspirators used to was 9,807 items, which gave a proportion of 0.02

carry out the fraud. Their end-of-days method, (9,807 ÷ 493,621 records). The Benford’s Law

which he called “Rabbits pulled out of hats,” in- proportions range from a high of 0.0414 for the

volved calculating the pro forma earnings at the end 10 on the left side of the graph, down to a low of

of each quarter, identifying “the hole” (the shortfall 0.0044 for the 99 on the right side of the graph.

between the actual and the desired earnings), and As the first-two digits increase (10, 11, 12, …, 99),

then filling the hole with “dirt” (fictitious journal the expected proportions decrease. Where the

entries to eliminate the shortfall). The shortfall top of the bar touches the line, it means that the

IN BRIEF identify ridges and valleys in data: as unusually high duplications of same-

ranges in a graph where data clusters dollar transactions. These irregularities

■ Benford’s Law can be used to identify over or under the Benford’s Law line. are not necessarily indicators of fraud.

large counts of fictitious journal entries Such ridges and valleys can be signs ■ Auditors can look for spikes in data that

that are below the auditor’s testing that large numbers of fictitious entries rise above a threshold line to pinpoint

threshold. These fictitious journal have been created. irregularities that require further

entries can be a fraud method. ■ Benford’s Law can also identify investigation.

■ Auditors can use the Runs test to irregularities in the general ledger such

To comment on this article or to suggest an idea for another article, contact Courtney Vien at Courtney.Vien@aicpa-cima.com.

14 | Journal of Accountancy September 2022