Page 372 - JoFA_2022

P. 372

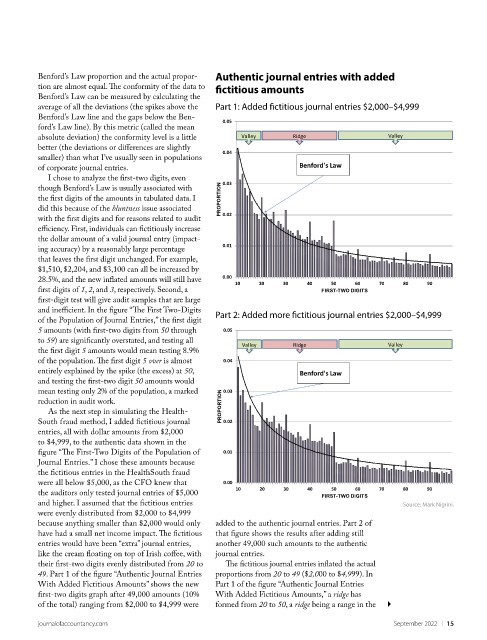

Authentic journal entries with added

Benford’s Law proportion and the actual propor-

fictitious amounts

tion are almost equal. The conformity of the data to

Benford’s Law can be measured by calculating the

average of all the deviations (the spikes above the Part 1: Added fictitious journal entries $2,000–$4,999

Benford’s Law line and the gaps below the Ben-

0.05

ford’s Law line). By this metric (called the mean

absolute deviation) the conformity level is a little Valley Ridge Valley

better (the deviations or differences are slightly

0.04

smaller) than what I’ve usually seen in populations

Benford's Law

of corporate journal entries.

I chose to analyze the first-two digits, even

though Benford’s Law is usually associated with 0.03

the first digits of the amounts in tabulated data. I PROPORTION

did this because of the bluntness issue associated 0.02

with the first digits and for reasons related to audit

efficiency. First, individuals can fictitiously increase

the dollar amount of a valid journal entry (impact-

0.01

ing accuracy) by a reasonably large percentage

that leaves the first digit unchanged. For example,

$1,510, $2,204, and $3,100 can all be increased by

0.00

28.5%, and the new inflated amounts will still have

10 20 30 40 50 60 70 80 90

first digits of 1, 2, and 3, respectively. Second, a FIRST-TWO DIGITS

first-digit test will give audit samples that are large

and inefficient. In the figure “The First Two-Digits Part 2: Added more fictitious journal entries $2,000–$4,999

of the Population of Journal Entries,” the first digit

5 amounts (with first-two digits from 50 through 0.05

to 59) are significantly overstated, and testing all

Valley Ridge Valley

the first digit 5 amounts would mean testing 8.9%

of the population. The first digit 5 over is almost 0.04

entirely explained by the spike (the excess) at 50, Benford's Law

and testing the first-two digit 50 amounts would

mean testing only 2% of the population, a marked 0.03

reduction in audit work. PROPORTION

As the next step in simulating the Health-

South fraud method, I added fictitious journal 0.02

entries, all with dollar amounts from $2,000

to $4,999, to the authentic data shown in the

figure “The First-Two Digits of the Population of 0.01

Journal Entries.” I chose these amounts because

the fictitious entries in the HealthSouth fraud

were all below $5,000, as the CFO knew that 0.00

10 20 30 40 50 60 70 80 90

the auditors only tested journal entries of $5,000 FIRST-TWO DIGITS

and higher. I assumed that the fictitious entries Source: Mark Nigrini.

were evenly distributed from $2,000 to $4,999

because anything smaller than $2,000 would only added to the authentic journal entries. Part 2 of

have had a small net income impact. The fictitious that figure shows the results after adding still

entries would have been “extra” journal entries, another 49,000 such amounts to the authentic

like the cream floating on top of Irish coffee, with journal entries.

their first-two digits evenly distributed from 20 to The fictitious journal entries inflated the actual

49. Part 1 of the figure “Authentic Journal Entries proportions from 20 to 49 ($2,000 to $4,999). In

With Added Fictitious Amounts” shows the new Part 1 of the figure “Authentic Journal Entries

first-two digits graph after 49,000 amounts (10% With Added Fictitious Amounts,” a ridge has

of the total) ranging from $2,000 to $4,999 were formed from 20 to 50, a ridge being a range in the

journalofaccountancy.com September 2022 | 15