Page 375 - JoFA_2022

P. 375

FRAUD / AUDITING

The first-two digits of the invoice amounts data analytics will be at detecting a below-the-

testing-threshold fraud scheme, provided that the

follow-up audit work is done competently.

BENFORD’S LAW-BASED AUDIT PLANNING

AU-C Section 315, Understanding the Entity and

Its Environment and Assessing the Risks of Material

Misstatement, requires auditors to identify journal

entries that might represent specific risks, including

unusual transactions, events, amounts, ratios, and

trends. Benford’s Law-based audit analytics can also

be used to identify unusual transactions in journal

entries, as I demonstrate in the following example.

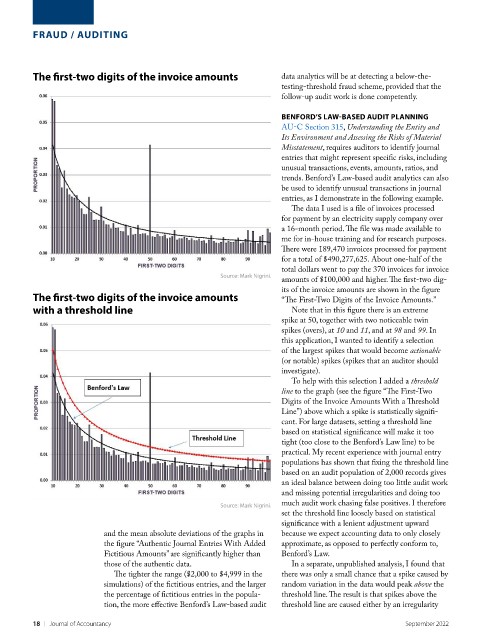

The data I used is a file of invoices processed

for payment by an electricity supply company over

a 16-month period. The file was made available to

me for in-house training and for research purposes.

There were 189,470 invoices processed for payment

for a total of $490,277,625. About one-half of the

total dollars went to pay the 370 invoices for invoice

Source: Mark Nigrini.

amounts of $100,000 and higher. The first-two dig-

its of the invoice amounts are shown in the figure

The first-two digits of the invoice amounts “The First-Two Digits of the Invoice Amounts.”

with a threshold line Note that in this figure there is an extreme

spike at 50, together with two noticeable twin

spikes (overs), at 10 and 11, and at 98 and 99. In

this application, I wanted to identify a selection

of the largest spikes that would become actionable

(or notable) spikes (spikes that an auditor should

investigate).

To help with this selection I added a threshold

line to the graph (see the figure “The First-Two

Digits of the Invoice Amounts With a Threshold

Line”) above which a spike is statistically signifi-

cant. For large datasets, setting a threshold line

based on statistical significance will make it too

tight (too close to the Benford’s Law line) to be

practical. My recent experience with journal entry

populations has shown that fixing the threshold line

based on an audit population of 2,000 records gives

an ideal balance between doing too little audit work

and missing potential irregularities and doing too

Source: Mark Nigrini. much audit work chasing false positives. I therefore

set the threshold line loosely based on statistical

significance with a lenient adjustment upward

and the mean absolute deviations of the graphs in because we expect accounting data to only closely

the figure “Authentic Journal Entries With Added approximate, as opposed to perfectly conform to,

Fictitious Amounts” are significantly higher than Benford’s Law.

those of the authentic data. In a separate, unpublished analysis, I found that

The tighter the range ($2,000 to $4,999 in the there was only a small chance that a spike caused by

simulations) of the fictitious entries, and the larger random variation in the data would peak above the

the percentage of fictitious entries in the popula- threshold line. The result is that spikes above the

tion, the more effective Benford’s Law-based audit threshold line are caused either by an irregularity

18 | Journal of Accountancy September 2022