Page 122 - ACFE Fraud Reports 2009_2020

P. 122

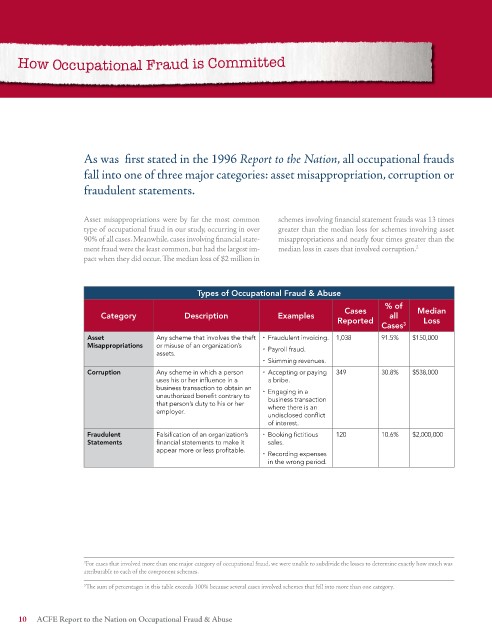

How Occupational Fraud is Committed

As was first stated in the 1996 Report to the Nation, all occupational frauds

fall into one of three major categories: asset misappropriation, corruption or

fraudulent statements.

Asset misappropriations were by far the most common schemes involving financial statement frauds was 13 times

type of occupational fraud in our study, occurring in over greater than the median loss for schemes involving asset

90% of all cases. Meanwhile, cases involving financial state- misappropriations and nearly four times greater than the

ment fraud were the least common, but had the largest im- median loss in cases that involved corruption.

2

pact when they did occur. The median loss of $2 million in

Types of Occupational Fraud & Abuse

% of

Cases Median

Category Description Examples all

Reported Loss

Cases 3

Asset Any scheme that involves the theft ¨ fraudulent invoicing. 1,038 91.5% $150,000

Misappropriations or misuse of an organization’s Payroll fraud.

assets. ¨

¨ Skimming revenues.

Corruption Any scheme in which a person ¨ Accepting or paying 349 30.8% $538,000

uses his or her influence in a a bribe.

business transaction to obtain an engaging in a

unauthorized benefit contrary to ¨ business transaction

that person’s duty to his or her where there is an

employer.

undisclosed conflict

of interest.

Fraudulent falsification of an organization’s ¨ Booking fictitious 120 10.6% $2,000,000

Statements financial statements to make it sales.

appear more or less profitable.

¨ Recording expenses

in the wrong period.

2 For cases that involved more than one major category of occupational fraud, we were unable to subdivide the losses to determine exactly how much was

attributable to each of the component schemes.

3 The sum of percentages in this table exceeds 100% because several cases involved schemes that fell into more than one category.

10 ACFE Report to the Nation on Occupational Fraud & Abuse