Page 123 - ACFE Fraud Reports 2009_2020

P. 123

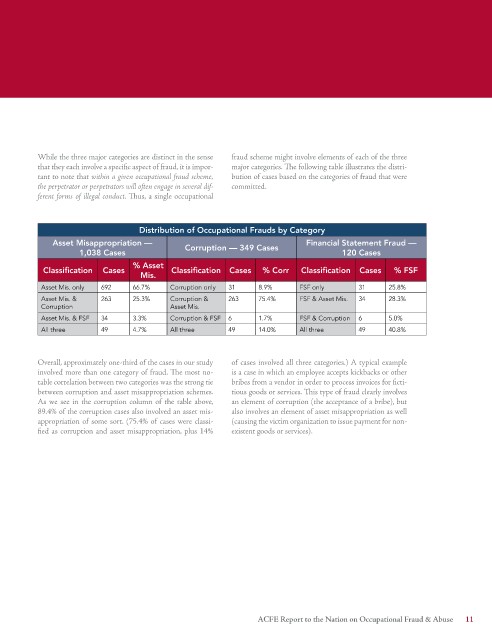

While the three major categories are distinct in the sense fraud scheme might involve elements of each of the three

that they each involve a specific aspect of fraud, it is impor- major categories. The following table illustrates the distri-

tant to note that within a given occupational fraud scheme, bution of cases based on the categories of fraud that were

the perpetrator or perpetrators will often engage in several dif- committed.

ferent forms of illegal conduct. Thus, a single occupational

Distribution of Occupational Frauds by Category

Asset Misappropriation — Corruption — 349 Cases Financial Statement Fraud —

1,038 Cases 120 Cases

% Asset

Classification Cases Classification Cases % Corr Classification Cases % FSF

Mis.

Asset Mis. only 692 66.7% corruption only 31 8.9% fSf only 31 25.8%

Asset Mis. & 263 25.3% corruption & 263 75.4% fSf & Asset Mis. 34 28.3%

corruption Asset Mis.

Asset Mis. & fSf 34 3.3% corruption & fSf 6 1.7% fSf & corruption 6 5.0%

All three 49 4.7% All three 49 14.0% All three 49 40.8%

Overall, approximately one-third of the cases in our study of cases involved all three categories.) A typical example

involved more than one category of fraud. The most no- is a case in which an employee accepts kickbacks or other

table correlation between two categories was the strong tie bribes from a vendor in order to process invoices for ficti-

between corruption and asset misappropriation schemes. tious goods or services. This type of fraud clearly involves

As we see in the corruption column of the table above, an element of corruption (the acceptance of a bribe), but

89.4% of the corruption cases also involved an asset mis- also involves an element of asset misappropriation as well

appropriation of some sort. (75.4% of cases were classi- (causing the victim organization to issue payment for non-

fied as corruption and asset misappropriation, plus 14% existent goods or services).

ACFE Report to the Nation on Occupational Fraud & Abuse 11