Page 140 - ACFE Fraud Reports 2009_2020

P. 140

Detecting Occupational Fraud

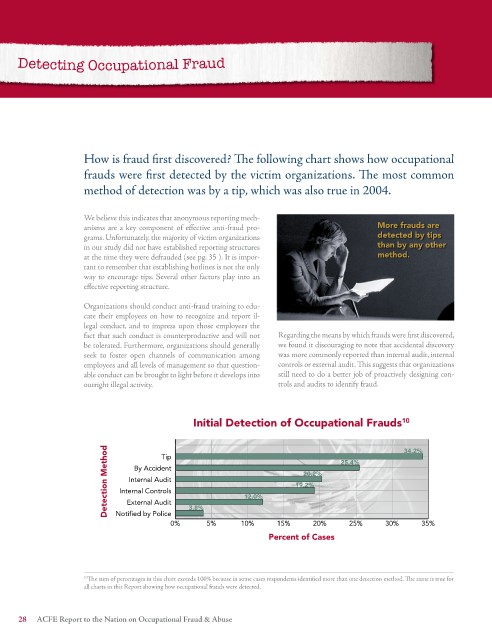

How is fraud first discovered? The following chart shows how occupational

frauds were first detected by the victim organizations. The most common

method of detection was by a tip, which was also true in 2004.

We believe this indicates that anonymous reporting mech-

anisms are a key component of effective anti-fraud pro- More frauds are

grams. Unfortunately, the majority of victim organizations detected by tips

in our study did not have established reporting structures than by any other

at the time they were defrauded (see pg. 35 ). It is impor- method.

tant to remember that establishing hotlines is not the only

way to encourage tips. Several other factors play into an

effective reporting structure.

Organizations should conduct anti-fraud training to edu-

cate their employees on how to recognize and report il-

legal conduct, and to impress upon those employees the

fact that such conduct is counterproductive and will not Regarding the means by which frauds were first discovered,

be tolerated. Furthermore, organizations should generally we found it discouraging to note that accidental discovery

seek to foster open channels of communication among was more commonly reported than internal audit, internal

employees and all levels of management so that question- controls or external audit. This suggests that organizations

able conduct can be brought to light before it develops into still need to do a better job of proactively designing con-

outright illegal activity. trols and audits to identify fraud.

Initial Detection of Occupational Frauds 10

Detection Method Internal Controls 12.0% 19.2% 25.4%

34.2%

Tip

By Accident

20.2%

Internal Audit

External Audit

Notified by Police

0% 3.8% 5% 10% 15% 20% 25% 30% 35%

Percent of Cases

10 The sum of percentages in this chart exceeds 100% because in some cases respondents identified more than one detection method. The same is true for

all charts in this Report showing how occupational frauds were detected.

ACFE Report to the Nation on Occupational Fraud & Abuse