Page 142 - ACFE Fraud Reports 2009_2020

P. 142

Detecting Occupational Fraud

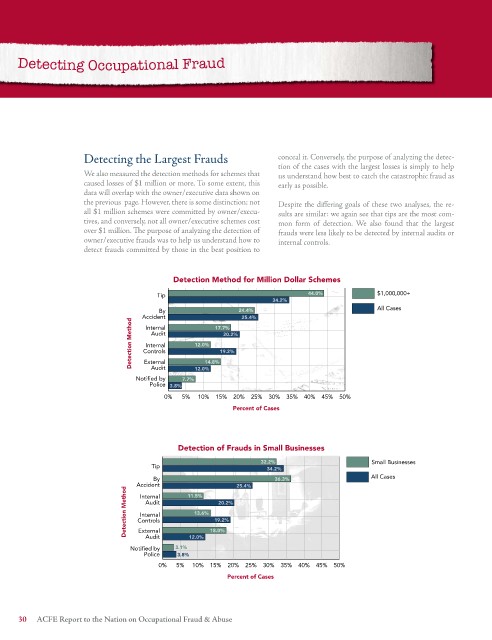

Detecting the Largest Frauds conceal it. Conversely, the purpose of analyzing the detec-

tion of the cases with the largest losses is simply to help

We also measured the detection methods for schemes that us understand how best to catch the catastrophic fraud as

caused losses of $1 million or more. To some extent, this early as possible.

data will overlap with the owner/executive data shown on

the previous page. However, there is some distinction; not Despite the differing goals of these two analyses, the re-

all $1 million schemes were committed by owner/execu- sults are similar: we again see that tips are the most com-

tives, and conversely, not all owner/executive schemes cost mon form of detection. We also found that the largest

over $1 million. The purpose of analyzing the detection of frauds were less likely to be detected by internal audits or

owner/executive frauds was to help us understand how to internal controls.

detect frauds committed by those in the best position to

Detection Method for Million Dollar Schemes

Tip 44.0% $1,000,000+

34.2%

By 24.4% All Cases

Accident 17.7% 25.4%

Detection Method Controls 12.0% 19.2%

Internal

Audit

20.2%

Internal

External

14.8%

Audit

Notified by 7.7% 12.0%

Police 3.8%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Percent of Cases

Detection of Frauds in Small Businesses

32.2% Small Businesses

Tip 34.2%

By 36.3% All Cases

Accident 11.5% 25.4%

Detection Method Controls 13.6% 18.0%

Internal

Audit

20.2%

Internal

19.2%

External

Audit

Notified by 3.1% 12.0%

Police 3.8%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Percent of Cases

0 ACFE Report to the Nation on Occupational Fraud & Abuse