Page 141 - ACFE Fraud Reports 2009_2020

P. 141

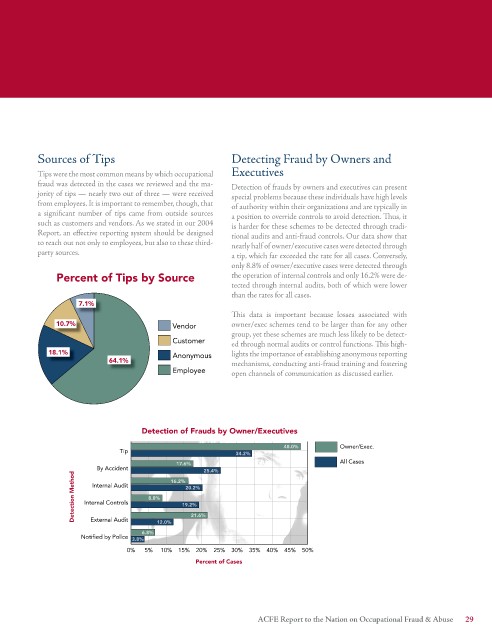

Sources of Tips Detecting Fraud by Owners and

Tips were the most common means by which occupational Executives

fraud was detected in the cases we reviewed and the ma- Detection of frauds by owners and executives can present

jority of tips — nearly two out of three — were received special problems because these individuals have high levels

from employees. It is important to remember, though, that of authority within their organizations and are typically in

a significant number of tips came from outside sources a position to override controls to avoid detection. Thus, it

such as customers and vendors. As we stated in our 2004 is harder for these schemes to be detected through tradi-

Report, an effective reporting system should be designed tional audits and anti-fraud controls. Our data show that

to reach out not only to employees, but also to these third- nearly half of owner/executive cases were detected through

party sources. a tip, which far exceeded the rate for all cases. Conversely,

only 8.8% of owner/executive cases were detected through

Percent of Tips by Source the operation of internal controls and only 16.2% were de-

tected through internal audits, both of which were lower

than the rates for all cases.

7.1%

This data is important because losses associated with

10.7% Vendor owner/exec schemes tend to be larger than for any other

group, yet these schemes are much less likely to be detect-

Customer ed through normal audits or control functions. This high-

18.1% Anonymous lights the importance of establishing anonymous reporting

64.1% mechanisms, conducting anti-fraud training and fostering

Employee open channels of communication as discussed earlier.

Detection of Frauds by Owner/Executives

48.0% Owner/Exec. Cases

Tip 34.2%

All Cases

17.6%

By Accident 16.2% 25.4%

Detection Method Internal Controls 8.8% 19.2%

Internal Audit

20.2%

21.6%

External Audit

6.8% 12.0%

Notified by Police 3.8%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Percent of Cases

ACFE Report to the Nation on Occupational Fraud & Abuse