Page 149 - ACFE Fraud Reports 2009_2020

P. 149

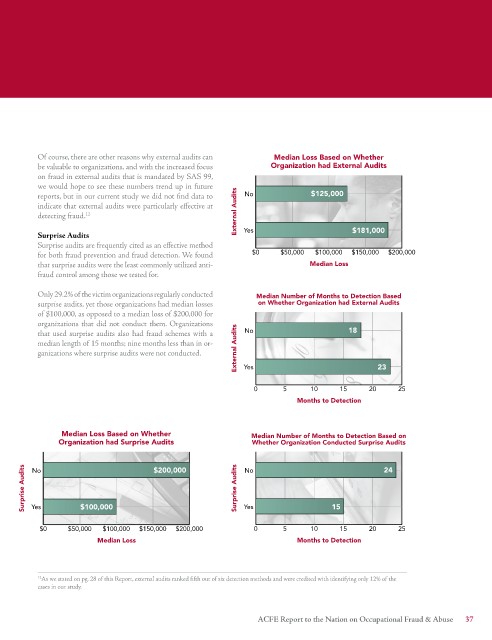

Of course, there are other reasons why external audits can Median Loss Based on Whether

be valuable to organizations, and with the increased focus Organization had External Audits

on fraud in external audits that is mandated by SAS 99,

we would hope to see these numbers trend up in future

reports, but in our current study we did not find data to No $125,000

indicate that external audits were particularly effective at

detecting fraud. 12 External Audits

Surprise Audits Yes $181,000

Surprise audits are frequently cited as an effective method

for both fraud prevention and fraud detection. We found $0 $50,000 $100,000 $150,000 $200,000

that surprise audits were the least commonly utilized anti- Median Loss

fraud control among those we tested for.

Only 29.2% of the victim organizations regularly conducted Median Number of Months to Detection Based

surprise audits, yet those organizations had median losses on Whether Organization had External Audits

of $100,000, as opposed to a median loss of $200,000 for

organizations that did not conduct them. Organizations

that used surprise audits also had fraud schemes with a No 18

median length of 15 months; nine months less than in or-

ganizations where surprise audits were not conducted. External Audits Yes 23

0 5 10 15 20 25

Months to Detection

Median Loss Based on Whether Median Number of Months to Detection Based on

Organization had Surprise Audits Whether Organization Conducted Surprise Audits

Surprise Audits No $100,000 $200,000 Surprise Audits Yes 15 24

No

Yes

$0 $50,000 $100,000 $150,000 $200,000 0 5 10 15 20 25

Median Loss Months to Detection

12 As we stated on pg. 28 of this Report, external audits ranked fifth out of six detection methods and were credited with identifying only 12% of the

cases in our study.

ACFE Report to the Nation on Occupational Fraud & Abuse