Page 151 - ACFE Fraud Reports 2009_2020

P. 151

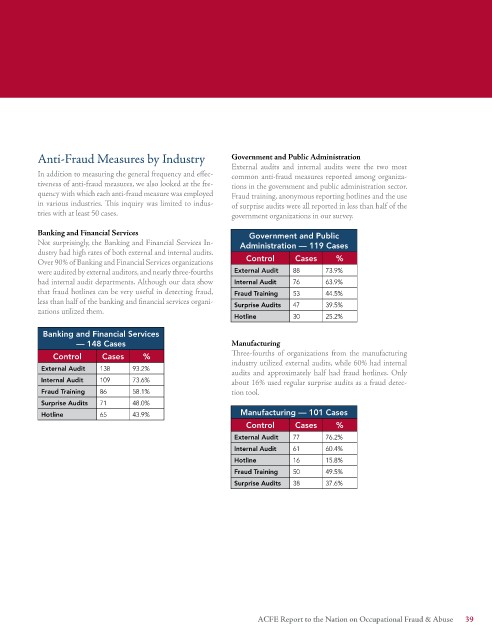

Anti-Fraud Measures by Industry Government and Public Administration

External audits and internal audits were the two most

In addition to measuring the general frequency and effec- common anti-fraud measures reported among organiza-

tiveness of anti-fraud measures, we also looked at the fre- tions in the government and public administration sector.

quency with which each anti-fraud measure was employed Fraud training, anonymous reporting hotlines and the use

in various industries. This inquiry was limited to indus- of surprise audits were all reported in less than half of the

tries with at least 50 cases. government organizations in our survey.

Banking and Financial Services Government and Public

Not surprisingly, the Banking and Financial Services In- Administration — 119 Cases

dustry had high rates of both external and internal audits.

Over 90% of Banking and Financial Services organizations Control Cases %

were audited by external auditors, and nearly three-fourths External Audit 88 73.9%

had internal audit departments. Although our data show Internal Audit 76 63.9%

that fraud hotlines can be very useful in detecting fraud, Fraud Training 53 44.5%

less than half of the banking and financial services organi- Surprise Audits 47 39.5%

zations utilized them.

Hotline 30 25.2%

Banking and Financial Services

— 148 Cases Manufacturing

Control Cases % Three-fourths of organizations from the manufacturing

industry utilized external audits, while 60% had internal

External Audit 138 93.2%

audits and approximately half had fraud hotlines. Only

Internal Audit 109 73.6% about 16% used regular surprise audits as a fraud detec-

Fraud Training 86 58.1% tion tool.

Surprise Audits 71 48.0%

Hotline 65 43.9% Manufacturing — 101 Cases

Control Cases %

External Audit 77 76.2%

Internal Audit 61 60.4%

Hotline 16 15.8%

Fraud Training 50 49.5%

Surprise Audits 38 37.6%

ACFE Report to the Nation on Occupational Fraud & Abuse 39