Page 153 - ACFE Fraud Reports 2009_2020

P. 153

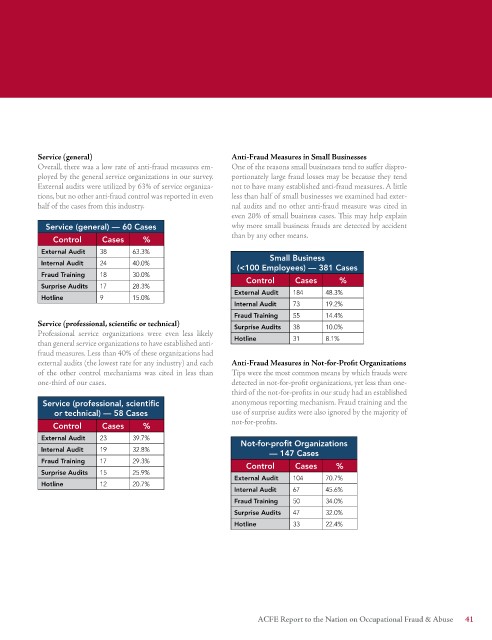

Service (general) Anti-Fraud Measures in Small Businesses

Overall, there was a low rate of anti-fraud measures em- One of the reasons small businesses tend to suffer dispro-

ployed by the general service organizations in our survey. portionately large fraud losses may be because they tend

External audits were utilized by 63% of service organiza- not to have many established anti-fraud measures. A little

tions, but no other anti-fraud control was reported in even less than half of small businesses we examined had exter-

half of the cases from this industry. nal audits and no other anti-fraud measure was cited in

even 20% of small business cases. This may help explain

Service (general) — 60 Cases why more small business frauds are detected by accident

than by any other means.

Control Cases %

External Audit 38 63.3% Small Business

Internal Audit 24 40.0% (<100 Employees) — 381 Cases

Fraud Training 18 30.0%

Control Cases %

Surprise Audits 17 28.3%

External Audit 184 48.3%

Hotline 9 15.0%

Internal Audit 73 19.2%

Fraud Training 55 14.4%

Service (professional, scientific or technical) Surprise Audits 38 10.0%

Professional service organizations were even less likely

than general service organizations to have established anti- Hotline 31 8.1%

fraud measures. Less than 40% of these organizations had

external audits (the lowest rate for any industry) and each Anti-Fraud Measures in Not-for-Profit Organizations

of the other control mechanisms was cited in less than Tips were the most common means by which frauds were

one-third of our cases. detected in not-for-profit organizations, yet less than one-

third of the not-for-profits in our study had an established

Service (professional, scientific anonymous reporting mechanism. Fraud training and the

or technical) — 58 Cases use of surprise audits were also ignored by the majority of

not-for-profits.

Control Cases %

External Audit 23 39.7% Not-for-profit Organizations

Internal Audit 19 32.8% — 147 Cases

Fraud Training 17 29.3%

Control Cases %

Surprise Audits 15 25.9%

External Audit 104 70.7%

Hotline 12 20.7%

Internal Audit 67 45.6%

Fraud Training 50 34.0%

Surprise Audits 47 32.0%

Hotline 33 22.4%

ACFE Report to the Nation on Occupational Fraud & Abuse 1