Page 218 - ACFE Fraud Reports 2009_2020

P. 218

4 Victim organizations

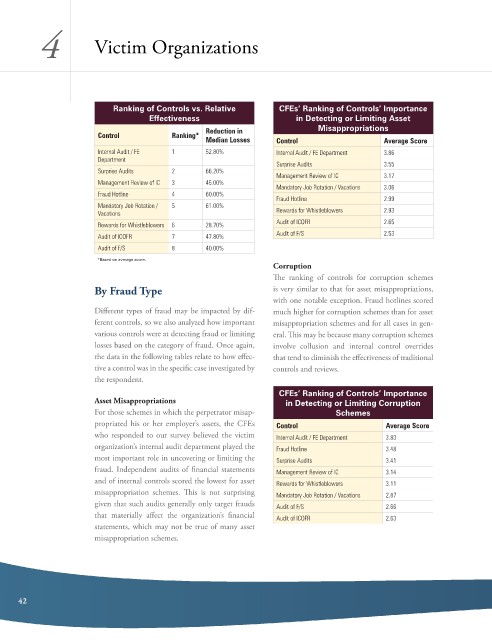

Ranking of Controls vs. Relative CFEs’ Ranking of Controls’ Importance

Effectiveness in Detecting or Limiting Asset

Reduction in Misappropriations

Control Ranking*

Median Losses Control Average Score

Internal Audit / FE 1 52.80% Internal Audit / FE Department 3.86

Department

Surprise Audits 3.55

Surprise Audits 2 66.20%

Management Review of IC 3.17

Management Review of IC 3 45.00%

Mandatory Job Rotation / Vacations 3.06

Fraud Hotline 4 60.00%

Fraud Hotline 2.99

Mandatory Job Rotation / 5 61.00%

Vacations Rewards for Whistleblowers 2.93

Rewards for Whistleblowers 6 28.70% Audit of ICOFR 2.65

Audit of ICOFR 7 47.80% Audit of F/S 2.53

Audit of F/S 8 40.00%

*Based on average score.

Corruption

The ranking of controls for corruption schemes

By Fraud Type is very similar to that for asset misappropriations,

with one notable exception. Fraud hotlines scored

different types of fraud may be impacted by dif- much higher for corruption schemes than for asset

ferent controls, so we also analyzed how important misappropriation schemes and for all cases in gen-

various controls were at detecting fraud or limiting eral. This may be because many corruption schemes

losses based on the category of fraud. once again, involve collusion and internal control overrides

the data in the following tables relate to how effec- that tend to diminish the effectiveness of traditional

tive a control was in the specific case investigated by controls and reviews.

the respondent.

CFEs’ Ranking of Controls’ Importance

Asset Misappropriations in Detecting or Limiting Corruption

For those schemes in which the perpetrator misap- Schemes

propriated his or her employer’s assets, the cFes Control Average Score

who responded to our survey believed the victim Internal Audit / FE Department 3.83

organization’s internal audit department played the Fraud Hotline 3.48

most important role in uncovering or limiting the Surprise Audits 3.41

fraud. independent audits of financial statements Management Review of IC 3.14

and of internal controls scored the lowest for asset Rewards for Whistleblowers 3.11

misappropriation schemes. This is not surprising Mandatory Job Rotation / Vacations 2.87

given that such audits generally only target frauds Audit of F/S 2.66

that materially affect the organization’s financial Audit of ICOFR 2.63

statements, which may not be true of many asset

misappropriation schemes.

42