Page 222 - ACFE Fraud Reports 2009_2020

P. 222

5 The perpetrators

We collected information about the individuals responsible for

occupational fraud in order to better understand the characteristics

of those who commit fraud and to see how certain types of fraud are

related to different job types or positions of authority.

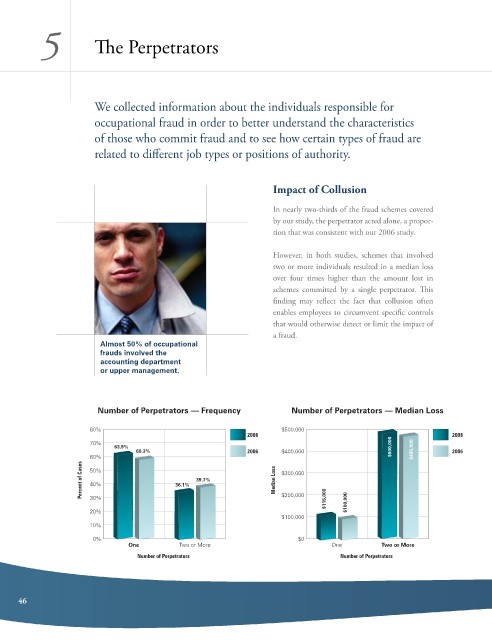

Impact of Collusion

in nearly two-thirds of the fraud schemes covered

by our study, the perpetrator acted alone, a propor-

tion that was consistent with our 2006 study.

However, in both studies, schemes that involved

two or more individuals resulted in a median loss

over four times higher than the amount lost in

schemes committed by a single perpetrator. This

finding may reflect the fact that collusion often

enables employees to circumvent specific controls

that would otherwise detect or limit the impact of

a fraud.

Almost 50% of occupational

frauds involved the

accounting department

or upper management.

Number of Perpetrators — Frequency Number of Perpetrators — Median Loss

80% $500,000

2008 2008

70%

63.9% $500,000

60.3% 2006 $400,000 $485,000 2006

60%

Percent of Cases 50% 36.1% 39.7% Median Loss $300,000

40%

$200,000

30%

20% $115,000 $100,000

$100,000

10%

0% $0

One Two or More One Two or More

Number of Perpetrators Number of Perpetrators

46