Page 221 - ACFE Fraud Reports 2009_2020

P. 221

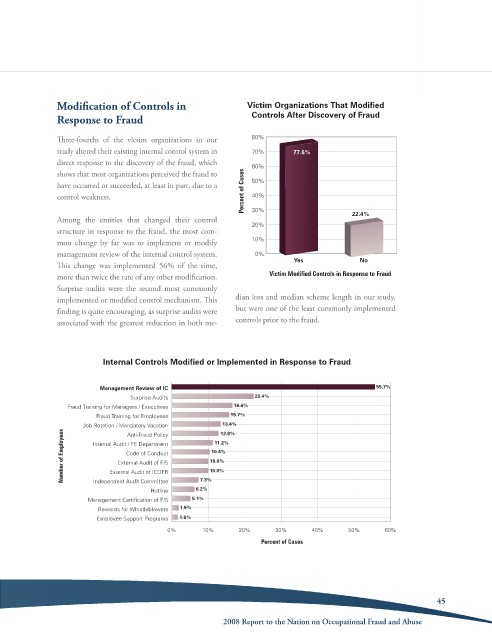

Modification of Controls in Victim Organizations That Modified

Response to Fraud Controls After Discovery of Fraud

Three-fourths of the victim organizations in our 80%

study altered their existing internal control system in 70% 77.6%

direct response to the discovery of the fraud, which 60%

shows that most organizations perceived the fraud to

have occurred or succeeded, at least in part, due to a 50%

control weakness. Percent of Cases 40%

among the entities that changed their control 30% 22.4%

20%

structure in response to the fraud, the most com-

mon change by far was to implement or modify 10%

management review of the internal control system. 0%

Yes No

This change was implemented 56% of the time,

more than twice the rate of any other modification. Victim Modified Controls in Response to Fraud

surprise audits were the second most commonly

implemented or modified control mechanism. This dian loss and median scheme length in our study,

finding is quite encouraging, as surprise audits were but were one of the least commonly implemented

associated with the greatest reduction in both me- controls prior to the fraud.

Internal Controls Modified or Implemented in Response to Fraud

Management Review of IC 55.7%

Surprise Audits 22.4%

Fraud Training for Managers / Executives 16.6%

Fraud Training for Employees 15.7%

13.4%

Job Rotation / Mandatory Vacation 12.8%

Number of Employees Internal Audit / FE Department 10.0%

Anti-Fraud Policy

11.2%

10.4%

Code of Conduct

External Audit of F/S

10.0%

External Audit of ICOFR

7.3%

Independent Audit Committee

Hotline 6.2%

Management Certification of F/S 5.1%

Rewards for Whistleblowers 1.9%

Employee Support Programs 1.6%

0% 10% 20% 30% 40% 50% 60%

Percent of Cases

45

2008 Report to the Nation on occupational Fraud and abuse