Page 549 - ACFE Fraud Reports 2009_2020

P. 549

Perpetrators

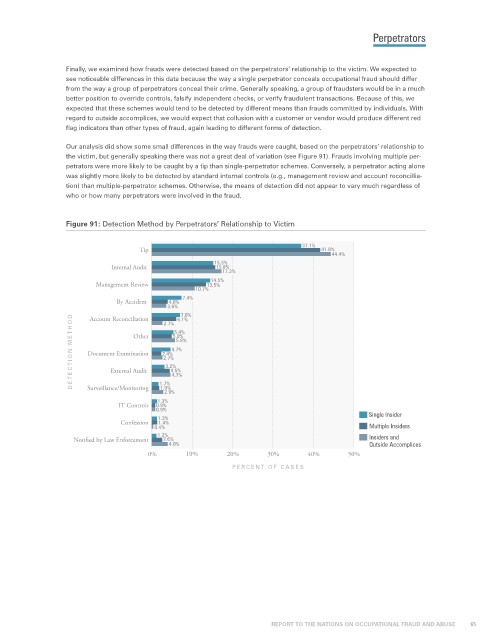

Finally, we examined how frauds were detected based on the perpetrators’ relationship to the victim. We expected to

see noticeable differences in this data because the way a single perpetrator conceals occupational fraud should differ

from the way a group of perpetrators conceal their crime. Generally speaking, a group of fraudsters would be in a much

better position to override controls, falsify independent checks, or verify fraudulent transactions. Because of this, we

expected that these schemes would tend to be detected by different means than frauds committed by individuals. With

regard to outside accomplices, we would expect that collusion with a customer or vendor would produce different red

flag indicators than other types of fraud, again leading to different forms of detection.

Our analysis did show some small differences in the way frauds were caught, based on the perpetrators’ relationship to

the victim, but generally speaking there was not a great deal of variation (see Figure 91). Frauds involving multiple per-

petrators were more likely to be caught by a tip than single-perpetrator schemes. Conversely, a perpetrator acting alone

was slightly more likely to be detected by standard internal controls (e.g., management review and account reconcillia-

tion) than multiple-perpetrator schemes. Otherwise, the means of detection did not appear to vary much regardless of

who or how many perpetrators were involved in the fraud.

Figure 91: Detection Method by Perpetrators’ Relationship to Victim

37.1%

Tip 41.8%

44.4%

15.3%

Internal Audit 15.8%

17.3%

14.5%

Management Review 13.5%

10.7%

7.4%

By Accident 4.0%

3.6%

7.0%

DETECTION METHOD Document Examination 2.4% 4.5%

Account Reconciliation

6.1%

2.7%

5.4%

Other

5.0%

5.8%

4.7%

2.7%

3.2%

External Audit

1.7%

Surveillance/Monitoring

1.9%

2.9% 4.7%

1.3%

IT Controls 0.9%

0.9%

1.3% Single Insider

Confession 1.4%

0.4% Multiple Insiders

1.2%

Notified by Law Enforcement 2.6% Insiders and

4.0% Outside Accomplices

0% 10% 20% 30% 40% 50%

PERCENT OF CASES

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 65