Page 548 - ACFE Fraud Reports 2009_2020

P. 548

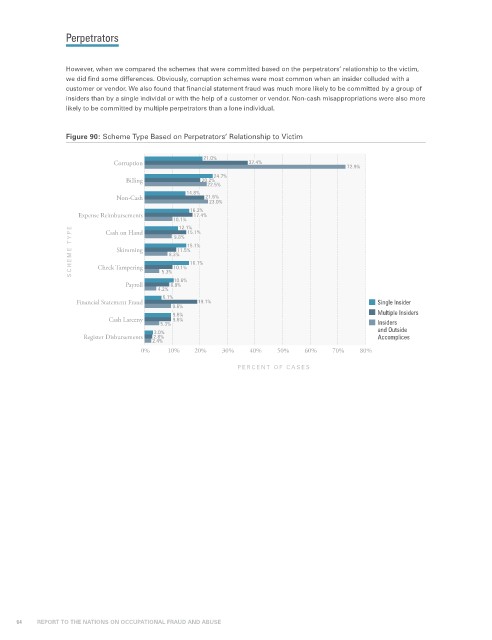

Perpetrators

However, when we compared the schemes that were committed based on the perpetrators’ relationship to the victim,

we did find some differences. Obviously, corruption schemes were most common when an insider colluded with a

customer or vendor. We also found that financial statement fraud was much more likely to be committed by a group of

insiders than by a single individal or with the help of a customer or vendor. Non-cash misappropriations were also more

likely to be committed by multiple perpetrators than a lone individual.

Figure 90: Scheme Type Based on Perpetrators’ Relationship to Victim

21.0%

Corruption 37.4%

72.9%

24.7%

Billing 20.2%

22.5%

14.8%

Non-Cash 21.6%

23.0%

16.2%

Expense Reimbursements 17.4%

10.1% 15.1%

12.1%

SCHEME TYPE Skimming 8.3% 11.5% 15.1%

Cash on Hand

9.8%

16.1%

Check Tampering

10.1%

5.3%

10.6%

Payroll 8.9%

4.2%

6.1%

Financial Statement Fraud 19.1% Single Insider

9.6%

9.6% Multiple Insiders

Cash Larceny 9.6%

5.3% Insiders

3.0% and Outside

Register Disbursements 2.8% Accomplices

2.4%

0% 10% 20% 30% 40% 50% 60% 70% 80%

PERCENT OF CASES

64 REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE