Page 608 - ACFE Fraud Reports 2009_2020

P. 608

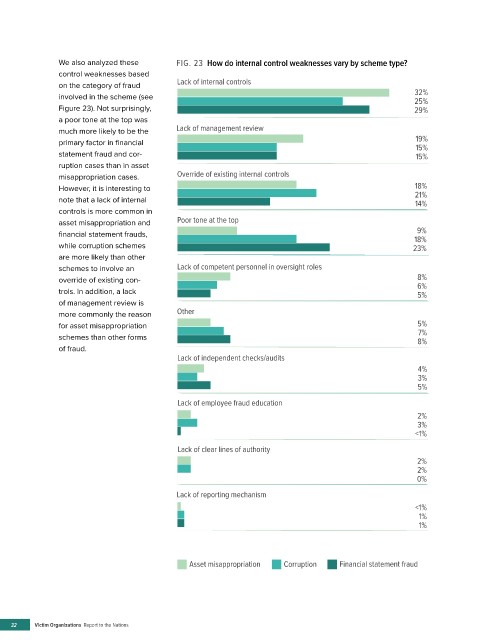

We also analyzed these FIG. 23 How do internal control weaknesses vary by scheme type?

control weaknesses based

on the category of fraud Lack of internal controls

involved in the scheme (see 32%

25%

Figure 23). Not surprisingly, 29%

a poor tone at the top was

much more likely to be the Lack of management review

primary factor in financial 19%

15%

statement fraud and cor- 15%

ruption cases than in asset

misappropriation cases. Override of existing internal controls

However, it is interesting to 18%

note that a lack of internal 21%

14%

controls is more common in

asset misappropriation and Poor tone at the top

9%

financial statement frauds, 18%

while corruption schemes 23%

are more likely than other

schemes to involve an Lack of competent personnel in oversight roles

override of existing con- 8%

6%

trols. In addition, a lack 5%

of management review is

more commonly the reason Other

for asset misappropriation 5%

schemes than other forms 7%

8%

of fraud.

Lack of independent checks/audits

4%

3%

5%

Lack of employee fraud education

2%

3%

<1%

Lack of clear lines of authority

2%

2%

0%

Lack of reporting mechanism

<1%

1%

1%

Asset misappropriation Corruption Financial statement fraud

32 Victim Organizations Report to the Nations