Page 609 - ACFE Fraud Reports 2009_2020

P. 609

PERPETRATORS

What does a typical fraudster look like?

We asked survey respondents to provide a broad range of information about

the fraud perpetrators they investigated, including the offenders’ conditions

of employment, basic demographics, prior misconduct, and behavior that

might have been warning signs of fraudulent activity. Our goal is to identify

common characteristics and risk profiles for those who commit occupational

fraud, which can help organizations better recognize fraud perpetrators or

those at risk for engaging in fraudulent activity.

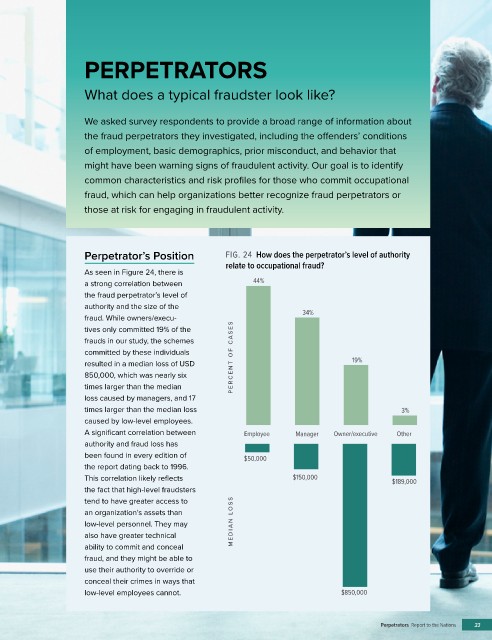

Perpetrator’s Position FIG. 24 How does the perpetrator’s level of authority

relate to occupational fraud?

As seen in Figure 24, there is

a strong correlation between 44%

the fraud perpetrator’s level of

authority and the size of the

fraud. While owners/execu- 34%

tives only committed 19% of the

frauds in our study, the schemes

committed by these individuals

resulted in a median loss of USD PERCENT OF C A SES 19%

850,000, which was nearly six

times larger than the median

loss caused by managers, and 17

times larger than the median loss 3%

caused by low-level employees.

A significant correlation between Employee Manager Owner/executive Other

authority and fraud loss has

been found in every edition of $50,000

the report dating back to 1996.

This correlation likely reflects $150,000 $189,000

the fact that high-level fraudsters

tend to have greater access to

an organization’s assets than

low-level personnel. They may MEDIAN L OSS

also have greater technical

ability to commit and conceal

fraud, and they might be able to

use their authority to override or

conceal their crimes in ways that

low-level employees cannot. $850,000

Perpetrators Report to the Nations 33