Page 614 - ACFE Fraud Reports 2009_2020

P. 614

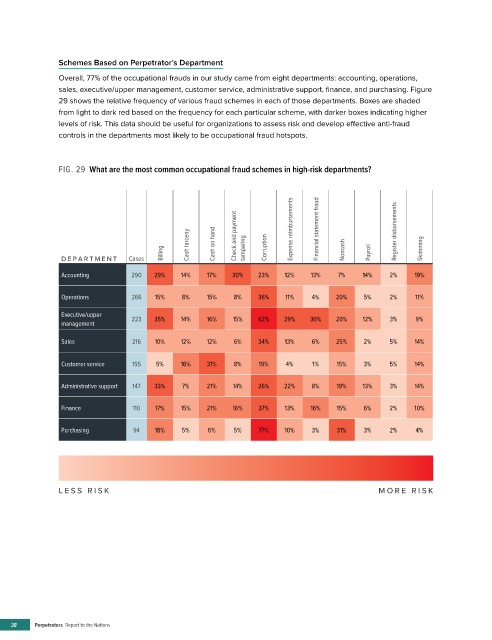

Schemes Based on Perpetrator’s Department

Overall, 77% of the occupational frauds in our study came from eight departments: accounting, operations,

sales, executive/upper management, customer service, administrative support, finance, and purchasing. Figure

29 shows the relative frequency of various fraud schemes in each of those departments. Boxes are shaded

from light to dark red based on the frequency for each particular scheme, with darker boxes indicating higher

levels of risk. This data should be useful for organizations to assess risk and develop effective anti-fraud

controls in the departments most likely to be occupational fraud hotspots.

FIG. 29 What are the most common occupational fraud schemes in high-risk departments?

Cash larceny Cash on hand Check and payment tampering Corruption Expense reimbursements Financial statement fraud Register disbursements Skimming

Billing Noncash Payroll

D E P A R T M E N T Cases

Accounting 290 29% 14% 17% 30% 23% 12% 13% 7% 14% 2% 19%

Operations 266 15% 8% 15% 8% 36% 11% 4% 20% 5% 2% 11%

Executive/upper 223 35% 14% 16% 15% 62% 29% 30% 20% 12% 3% 9%

management

Sales 216 10% 12% 12% 6% 34% 13% 6% 25% 2% 5% 14%

Customer service 155 5% 16% 31% 8% 19% 4% 1% 15% 3% 5% 14%

Administrative support 147 33% 7% 21% 14% 26% 22% 8% 19% 13% 3% 14%

Finance 110 17% 15% 21% 16% 37% 13% 16% 15% 6% 2% 10%

Purchasing 94 18% 5% 6% 5% 77% 10% 3% 31% 3% 2% 4%

LESS RISK MORE RISK

38 Perpetrators Report to the Nations