Page 20 - FSSI EE Guide 07-19 - flip

P. 20

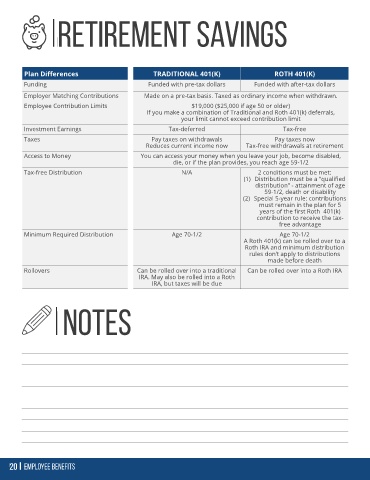

Plan Differences TRADITIONAL 401(K) ROTH 401(K)

Funding Funded with pre-tax dollars Funded with after-tax dollars

Employer Matching Contributions Made on a pre-tax basis. Taxed as ordinary income when withdrawn.

Employee Contribution Limits $19,000 ($25,000 if age 50 or older)

If you make a combination of Traditional and Roth 401(k) deferrals,

your limit cannot exceed contribution limit

Investment Earnings Tax-deferred Tax-free

Taxes Pay taxes on withdrawals Pay taxes now

Reduces current income now Tax-free withdrawals at retirement

Access to Money You can access your money when you leave your job, become disabled,

die, or if the plan provides, you reach age 59-1/2

Tax-free Distribution N/A 2 conditions must be met:

(1) Distribution must be a “qualified

distribution” - attainment of age

59-1/2, death or disability

(2) Special 5-year rule: contributions

must remain in the plan for 5

years of the first Roth 401(k)

contribution to receive the tax-

free advantage

Minimum Required Distribution Age 70-1/2 Age 70-1/2

A Roth 401(k) can be rolled over to a

Roth IRA and minimum distribution

rules don’t apply to distributions

made before death

Rollovers Can be rolled over into a traditional Can be rolled over into a Roth IRA

IRA. May also be rolled into a Roth

IRA, but taxes will be due