Page 4 - IKAK P7

P. 4

14

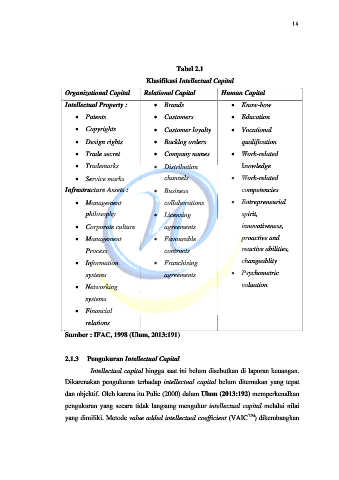

Tabel 2.1

Klasifikasi Intellectual Capital

Organizational Capital Relational Capital Human Capital

Intellectual Property : ∑ Brands ∑ Know-how

∑ Patents ∑ Customers ∑ Education

∑ Copyrights ∑ Customer loyalty ∑ Vocational

∑ Design rights ∑ Backlog orders qualification

∑ Trade secret ∑ Company names ∑ Work-related

∑ Trademarks ∑ Distribution knowledge

∑ Service marks channels ∑ Work-related

Infrastructure Assets : ∑ Business competencies

∑ Management collaborations ∑ Entrepreneurial

philosophy ∑ Licensing spirit,

∑ Corporate culture agreements innovativeness,

∑ Management ∑ Favourable proactive and

Process contracts reactive abilities,

∑ Information ∑ Franchising changeablity

systems agreements ∑ Psychometric

∑ Networking valuation

systems

∑ Financial

relations

Sumber : IFAC, 1998 (Ulum, 2013:191)

2.1.3 Pengukuran Intellectual Capital

Intellectual capital hingga saat ini belum disebutkan di laporan keuangan.

Dikarenakan pengukuran terhadap intellectual capital belum ditemukan yang tepat

dan objektif. Oleh karena itu Pulic (2000) dalam Ulum (2013:192) memperkenalkan

pengukuran yang secara tidak langsung mengukur intellectual capital melalui nilai

yang dimiliki. Metode value added intellectual coefficient (VAIC TM ) dikembangkan