Page 229 - Corporate Finance PDF Final new link

P. 229

NPP

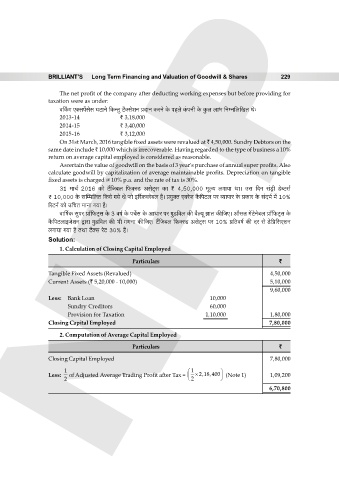

BRILLIANT’S Long Term Financing and Valuation of Goodwill & Shares 229

The net profit of the company after deducting working expenses but before providing for

taxation were as under:

d{Hª$J E³gn|gog KQ>mZo {H$ÝVw Q>¡³goeZ àXmZ H$aZo Ho$ nhbo H§$nZr Ho$ Hw$b bm^ {ZåZ{b{IV Wo…

2013-14 ` 3,18,000

2014-15 ` 3,40,000

2015-16 ` 3,12,000

On 31st March, 2016 tangible fixed assets were revalued at ` 4,50,000. Sundry Debtors on the

same date include ` 10,000 which is irrecoverable. Having regarded to the type of business a 10%

return on average capital employed is considered as reasonable.

Ascertain the value of goodwill on the basis of 3 year's purchase of annual super profits. Also

calculate goodwill by capitalization of average maintainable profits. Depreciation on tangible

fixed assets is charged @ 10% p.a. and the rate of tax is 30%.

31 ‘mM© 2016 H$mo Q>¢{O~b {’$³ñS> AgoQ²>g H$m < 4,50,000 ‘yë¶ bJm¶m Wm& Cg {XZ g§S´>r S>oãQ>g©

< 10,000 Ho$ gpå‘{bV {H$¶o J¶o Wo Omo B[a©H$dao~b h¡& à¶w³V EdaoO H¡${nQ>b na ì¶mnma Ho$ àH$ma Ho$ g§X^© ‘| 10%

[aQ>Z© H$mo C{MV ‘mZm J¶m h¡&

dm{f©H$ gwna àm°{’$Q²>g Ho$ 3 df© Ho$ nMo©g Ho$ AmYma na JwS>{db H$s d¡ë¶y kmV H$s{OE& Am¡gV ‘|Q>oZo~b àm°{’$Q²>g Ho$

H¡${nQ>bmBOoeZ Ûmam JwS>{db H$s ^r JUZm H$s{OE& Q>¢{O~b {’$³ñS> AgoQ²>g na 10% à{Vdf© H$s Xa go S>o{à{gEeZ

bJm¶m J¶m h¡ VWm Q>¡³g aoQ> 30% h¡&

Solution:

1. Calculation of Closing Capital Employed

Particulars `

Tangible Fixed Assets (Revalued) 4,50,000

Current Assets (` 5,20,000 - 10,000) 5,10,000

9,60,000

Less: Bank Loan 10,000

Sundry Creditors 60,000

Provision for Taxation 1,10,000 1,80,000

Closing Capital Employed 7,80,000

2. Computation of Average Capital Employed

Particulars `

Closing Capital Employed 7,80,000

1 1

Less: of Adjusted Average Trading Profit after Tax = 2,18,400 (Note 1) 1,09,200

2 2

6,70,800